The sun is shining bright on solar energy stocks in India.

The green energy sector is booming as India aims to achieve 500GW capacity of renewable energy by 2030. Investing in this sector is a promising opportunity for both seasoned investors and beginners. There are plenty of solar energy stocks to bring into your portfolio.

The Rise of Solar Energy In India

On 7th April 2021, The Union Cabinet approved the Production Linked Incentive (PLI) Scheme to boost the manufacturing of solar PV modules. The total of INR. 24,000 cr dedicated towards the sector aims to produce 39,600 MW capacity. India is set to create solar cities across the nation. The 1st solar city, ‘Sachi’, has already been launched in Madhya Pradesh in 2023. As the country marches ahead in this sector, many big solar panel manufacturers are raising INR. 5,800 cr this year. These funds will be used to establish 500 GW capacity by 2030. Along with Solar Panels, the manufacturers will also produce cells, wafers, and ingots under the PLI scheme.

We’ve handpicked a few solar energy companies that are available to invest. For recent share prices, get in touch with VNN Wealth. Read along to know more…

Top Unlisted Solar Energy Stocks in India: Upcoming IPOs in the Solar Sector

Apollo Green Energy Limited

Apollo Green Energy Limited (AGEL) is aiming to advance in the sustainable energy sector. Established in 1994, AGEL is owned by Apollo Group and has become a rising player in the green energy domain.

Apollo Green Energy Limited provides end-to-end solutions for green energy projects. Its specialty ranges across solar power, wind energy, biomass, and optimizing energy storage solutions. AGEL’s mission is to reduce carbon footprint by accompanying industries and communities to shift towards green energy resources through modern technologies.

The company has shown significant financial growth from 280 cr income in FY 2021 to 688 cr in 2023. AGEL is expected to generate 780 cr in review in FY 2024-25, 1380 cr in FY 20225-26, and cross over 2000 cr in 2026-27. The company is working on a wide range of projects and has a diverse portfolio. The projects under execution are smart solar street light installation, solar panel installation, thermal power project, and rural water supply project to name a few. The total value of the projects under execution is about 1735 cr. With promising growth, Apollo Green Energy Limited has become one of the leading companies in the renewable energy sector.

Vikram Solar

Update: Vikram Solar IPO: DRHP approved by NSE & BSE. The IPO is expected to debut at the beginning of 2025.

Vikram Solar is another big player in the green energy sector. With 3.5GW capacity, it is among the largest exporters of solar PV modules. Additionally, the company provides engineering, procurement, and construction (EPC) services, as well as operations and maintenance. Vikram Solar’s 70% of the revenue comes from PV modules and about 20% revenue comes from EPC. In the previous year, the company also received approval from the government to set up 2.4GW of additional capacity under the PLI scheme.

Currently, Vikram Solar is available to purchase in the unlisted market. The company has filed a draft with SEBI for an initial public offering (IPO). Vikram Solar IPO will offer a fresh issue of up to INR. 1,500 crores and an offer for sale of up to 5,000,000 equity shares.

Our Previous Recommendations

Waree Energies

Update: Waree Energies got listed on the stock market on Oct 28, 2024, at Rs. 2550, with a 70% premium over the issue price of 1503/share.

Waree Energies is playing a crucial role in expanding India’s renewable energy sector. The largest manufacturer of solar modules in India, Waree has rapidly boosted its capacity to 12GW in recent years. The company occupies about 50% of the market share in solar PV module export, surpassing Adani and Vikram Solar.

In December 2023, Waree Energies filed a draft with SEBI to raise INR. 3,000 crore through an initial public offering. The funds will be used to further expand the capacity from 12 GW to 38 GW over the next five years. Buying unlisted shares of Waree Energies can guarantee allocation and significant growth over the years. (Please note that the unlisted shares are subject to availability.)

Update: Premier Energies got listed on the stock market on Sept 3rd, 2024 with 120% premium over the issue price of 450/share.

Premier Energies is one of the largest integrated solar cells and solar module manufacturers in India. With 29 years spent in the solar sector, the company now has an installed capacity of 2GW for integrated solar cells and 3.36 GW for solar module manufacturing. Premier Energies has filed the draft with SEBI to raise INR. 1,500 crore via initial public offering (IPO).

The company will utilize INR. 1,168.74 to establish a 4 GW solar PV TOPCon cell and 4 GW solar PV TOPCon module manufacturing facility in Hyderabad. The remaining funds will go towards general corporate purposes. The company is also aiming to execute EPC projects, independent power production, and O&M services.

Final Thoughts

India’s solar energy sector is rapidly expanding with the PLI scheme in place. The government is taking the initiative to encourage growth in the capacity of renewable energy production. This is the right time to enter the sector by investing in solar energy stocks. It has the potential to deliver a significant return on your investment. Buying unlisted shares of Waree Energies or Vikram Solar will ensure allocation before the IPO. However, it is subject to availability. Get in touch with experts at VNN Wealth for the unlisted shares you wish to buy. Explore all unlisted shares here.

Unlisted shares in India have become popular over the past few years. Investors are buying unlisted shares of emerging companies showing potential growth as the awareness around them has increased.

By investing in these shares pre-IPO, you gain returns in two ways.

1. Prices of these shares may go up in the long run via over-the-counter trading.

2. You may bag pre-listing/ listing gains.

We’re receiving more inquiries about unlisted shares than ever before, especially after the Tata Tech IPO’s massive success. Tata Technologies was our second success story after Nazara Technologies in terms of entry and exit for our investors. And now, more unlisted companies have entered our top picks.

Interested to know which unlisted share to buy?

Our team of experts has curated a list of the top 8 unlisted shares in India.

Aiming to advance in the sustainable energy sector, Apollo Green Energy Limited (AGEL) is one of the rising players in India. Established in 1994, AGEL is owned by Apollo Group.

Apollo Green Energy Limited focuses on providing end-to-end solutions for green energy projects. Its specialty ranges across solar power, wind energy, biomass, and optimizing energy storage solutions. AGEL’s mission is to reduce carbon footprint by accompanying industries and communities to shift towards green energy resources via modern technologies.

The company has shown significant financial growth from 280 cr income in FY 2021 to 688 cr in 2023. AGEL is expected to generate 780 cr in review in FY 2024-25, 1380 cr in FY 20225-26, and cross over 2000 cr in 2026-27. Currently, the company is working on a wide range of projects, maintaining a diverse portfolio. The projects under execution are smart solar street light installation, solar panel installation, thermal power project, and rural water supply project to name a few. The total value of the projects under execution is approximately 1735 cr.

With promising growth, Apollo Green Energy Limited has become one of the leading companies in the renewable energy sector.

2. Vikram Solar Unlisted Shares

Founded in 2006, Vikram Solar is one of the leading solar PV module manufacturers in India. Currently, with 3.5 GW capacity, the company also provides integrated solar energy solutions, Engineering, Procurement, and Construction (EPC) services, and operations & maintenance. Vikram Solar has 3 manufacturing units in Tamilnadu and West Bengal. The company has 42+ distributors across 600 districts in India. Vikram’s 70% of revenue comes from PV modules and about 20% from EPC services.

It is the first company to contribute to fully solarizing Kochi(Kerala) airport, installing a floating solar plant in Kolkata, and commissioning large-scale rooftop solar plants across India. The company also has sales offices in the USA and has supplied solar PV modules in 32+ countries. The company’s revenue has increased to INR. 2015 crores in fy23, an 18% boost from the fy22 revenue. Vikram Solar has filed a draft with SEBI to raise INR. 1,500 crore via initial public offering (IPO) and an offer for sale of up to 5,000,000 equity shares.

3. TATA Capital Limited Unlisted Shares

A subsidiary of TATA Sons, TATA Capital Limited is registered with RBI as a non-deposit-accepting NBFC. Along with its subsidiaries, TATA Capital offers financial services to corporate, retail, and institutional customers. The company’s product portfolio includes various types of loans, investment advisory, cleantech finance, private equity, wealth products, commercial and SME finance, leasing solutions, and TATA cards, to name a few.

In the financial year 2022, TATA Capital reported the highest profit. The company’s PAT increased from INR 1,245 crore to INR 1,801 in FY22 crore and to INR 2,975 crore in FY23.Tata Capital’s loan book grew by 28% in FY22-23 and the book value increased to 48.36 from 33.82. The RoE also increased from 15.6% to 17.3%.

4. SBI Mutual Funds Unlisted Shares

SBI Funds Management Limited is one of the most popular, largest asset management firms in India. Founded in 1987, it’s a joint venture between the State Bank of India and AMUNDI (A global fund management company.) SBI currently holds a 63% stake and the remaining 37% belongs to AMUNDI. SBI mutual funds offer a wide range of mutual fund schemes such as equity mutual funds, debt funds, hybrid mutual funds, solution-oriented schemes, and Exchange-traded funds, to name a few. The company also launched an Alternative Investment Fund (AIF) in 2015 and may launch more funds in the future.

With over 53+ mutual funds schemes, SBI mutual funds have INR 1.65 trillion assets under management (AUM) and over 12 million investors.SBI fund management has been offering international investor solutions since 1988. The company guides and manages India’s dedicated offshore funds.The company also offers Portfolio Management services catering to HNIs, large provident funds, institutions, and selective trusts.

SBIFM’s AAUM is 44% more than the next largest peer (ICICI prudential mutual fund). And has hit a 27% CAGR when the rest of the market delivered 10% over a five-year horizon. As per the recent financial reports (March 2023), SBI fund management has made a net revenue of INR 2297.27 crores.

5. NSE India Limited Unlisted Shares

Founded in 1992, the National Stock Exchange (NSE) is India’s leading stock exchange with ~1968 companies listed on it.In 1994, NSE launched electronic screen-based trading, and internet trading in 2000. NSE’s flagship index, Nifty 50, serves as a global benchmark for Indian capital markets. NSE is the world’s largest derivative exchange with 21% of the global derivative contract trading. It’s also the second-largest derivatives exchange in the world for currency futures trading. The capital market business model of NSE primarily offers trading services, exchange listing, market data feeds, indices, and technology solutions.

Its cash market offers a platform to trade equity shares, mutual funds, ETFs, REITs, Sovereign Gold bonds, government securities, T-bills, etc. The debt market offers government, corporate bonds, commercial papers, and other debt instruments. NSE also provides index management services for equity indices, hybrid indices, and customized indices for asset management companies, insurance companies, investment banks, PMS, and stock exchanges.The company has performed at a CAGR of 35% over the last three years. NSE’s FY23 revenue has reached INR 12650 Cr. with a 63.27 net profit margin.

6. Chennai Super Kings

The four times IPL winner, CSK is the only sports team in India available for the general public to invest in.CSK is one of the most popular IPL franchises with a strong brand value. The brand was founded in 2008 as an IPL cricket team representing Chennai, Tamil Nadu. It is a wholly-owned subsidiary of India Cements.Being a popular IPL franchise, CSK became the country’s first sports unicorn. The brand’s market cap was raised to 7600 crores (more than 1 billion) with the share prices in the unlisted market trading between Rs. 210-225.

Chennai Super Kings generates revenues from various sources such as- Gate ticket collection, In-Stadium Advertisements, and Merchandise sales. The team earns 60% of the total revenue from Media Rights, which is the highest revenue stream. The revenue from sponsorship makes up around 15-20% of total revenue followed by 10% from ticket sales.While the Pandemic had an impact on many brands, CSK managed to maintain a balance via indirect revenue streams. One of the most loved IPL teams, CSK, will continue to generate solid revenue via merchandise sales, sponsorships, portions of prize money, and digital viewership.

7. Orbis Financials Corporation Unlisted Shares

Established in 2005, Orbis Financial Corporation Limited is a prominent company in India’s financial services sector. Orbis offers a wide range of services such as custody and fund accounting, equity derivatives clearing, currency derivatives clearing, share transfer agency and trustee services.

Orbis’s client base includes over 50 foreign portfolio investors (FPIs), 150 Alternative Investment Funds (AIFs), and more than 800 Non-Resident Indians (NRIs). The company earns revenue from custodial and clearing income and treasury-related income. It also generates income from the capital market.

In recent years, the company has shown excellent financial growth with a net profit of INR 89.57 cr in FY2023. Additionally, the company’s assets under custody (AUC) increased by 20% to ₹81,160 crore as of March 31, 2023.

The company’s share price increased by 76% over a span of a year as it climbed up to INR 125 by Sept 2023. Due to consistent performance, Orbis Financial Corporation unlisted share price stands at INR 475 as of Jan 2025 and has a potential for further growth.

8. Studds

Being a global leader in two-wheeler helmet manufacturing, Studds accounts for almost one-third share of the organized two-wheeler helmet market.Studds had an opportunity to manufacture face shields and protection wear in high demand during Covid-19. Studds’s sales received another boost when The Ministry of Road Transport and Highways declared that India would only manufacture and sell BIS-certified two-wheeler helmets.Demand for two-wheeler helmets is growing rapidly post-COVID-19 as transportation has resumed. Besides, people often replace their helmets within two to three years, enabling more business for the company.

Studds is also expanding its accessories manufacturing with riding gear gloves, goggles, jackets, and safety and storage gear.Additionally, Studds also has an opportunity to dominate bicycle helmet sales. The company is operating in more than 40 countries including Europe and US. Recently, the company has doubled its manufacturing capacity in Faridabad, Haryana.

Our Previous Recommendations

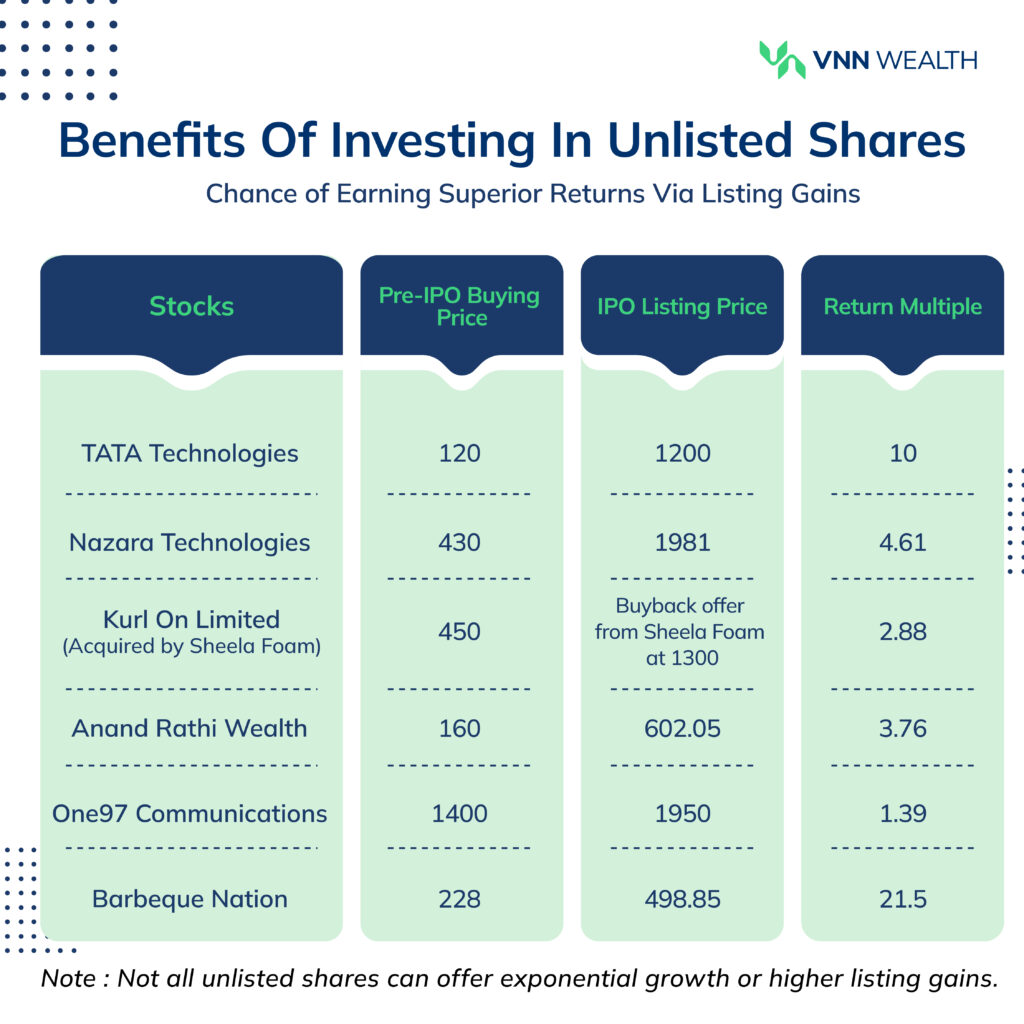

Nazara Technologies: Was listed on the stock exchange on March 30, 2021, at INR 1,981, an 81% boost from the issue price of INR 1,101.

TATA Technologies: Was listed on the stock exchange on 30th November, 2023 at INR 1,200, a whopping 140% higher than the issue price of INR 500.

Kurl On: In July 2023, Kurl On’s biggest rival Sheela Foam acquired a 95% stake in the company and offered a buyback option to shareholders.

Waaree: Was listed on the stock exchange on Oct 28, 2024 at INR. 2550with a 70% premium over the issue price of 1503/share.

How to Invest In Unlisted Shares?

Unlisted shares are not available to invest via the established stock exchanges as they’re traded over the counter or via private platforms. If you want to buy unlisted shares of the above companies, get in touch with us anytime and our team will take care of the rest.

Buying unlisted shares is a great strategy to diversify your investment portfolio. These shares are fairly safer than listed shares due to less volatility. And the major benefit of investing pre-IPO is the allocation confirmation. With Unlisted shares, investors have the opportunity to gain either pre-listing gains or listing gains.

Share prices of unlisted companies often boost right before the IPO. With a huge demand in the unlisted market, you can sell your shares and earn pre-listing gains. Or, you can wait until the IPO is live and get profit from listing gains. Please note that the pre-listing and listing gains are subject to market risk. To avoid any risks, we have chosen known brands with high brand value and promising futures. Get in touch with us if you are interested in buying the above shares. Experts at VNN Wealth will guide you through the process.

The number of NRIs (Non-Resident Indians) considering returning to India after retirement is rising. Those who went abroad seeking career growth are now ready to return to the warmth of their home country post-retirement.

A survey conducted by SBNRI revealed that more than 60% of NRIs are planning to return to India.

1. 80% NRIs from Australia and Singapore

2. 75% of NRIs from the United States

3. 70% from the United Kingdom

4. 63% from Canada

The numbers are significant and it’s easy to understand why the NRIs want to return. India is a booming economy that offers incredible investment opportunities and a comfortable lifestyle. And it’s a home after all.

So, if you are an NRI planning to return to India after retirement, this blog is for you. Read along to know what you need to consider before returning.

Why are NRIs Returning to India After Retirement?

1. Emotional Aspects

Being closer to the family and community is one of the strongest reasons for many NRIs thinking of returning to India. After spending years in a foreign country building a career, it’s natural to feel that pull towards your homeland.

The opportunity to celebrate festivals with the family and create memories holds significant emotional value. The familiarity with the people, the cuisine, and the vibrant traditions offer a sense of belonging.

A house in a hometown or in a familiar city ensures security, social engagement with friends and family, and comfort.

All these things gain importance in one’s life as they near retirement.

2. Cost-effective and Fast Healthcare

One of the primary factors while planning for retirement is the healthcare cost. Medical bills may increase with age, causing a severe dent in your savings.

Compared to other countries, healthcare costs in India are significantly lower. An NRI on X (formerly Twitter) recently shared his experience- one of his family members only had to pay $50 (~4000rs) for 72+ medical tests which would have cost $10000 (~8.4 lakh rs) in the US without health insurance.

Moreover, the wait time for medical appointments is longer in many developed countries. India offers fast healthcare and has adapted advanced treatments and equipment. The medical infrastructure in India is rapidly growing, even in small towns. You get efficient and cost-effective healthcare.

3. Access to Affordable House Help

Being able to hire a domestic health is an underrated advantage of living in India. You can rely on your house help for daily chores such as cooking, cleaning, and running errands. While this luxury is available in other countries, it’s usually at a much higher cost.

You can easily hire staff in India. There are plenty of third-party services that send trained staff as per your needs at affordable prices.

House help is going to make your life comfortable and relaxing, so you can enjoy your golden years.

4. Cost of Living

The cost of living in India is much lower compared to other countries. With your financial corpus built over the years, you can live a comfortable life throughout. Plus India has become a smart country, making life easier.

A few simple examples are- paying via UPI even at small shops, ordering groceries in 10 minutes with discounts on various payment options, and healthcare tests at home at affordable prices. From your haircut to a dine-in at a fancy restaurant, everything will be cheaper compared to your current lifestyle.

5. Investment Opportunities

India is a growing economy with plenty of investment opportunities for financial growth. From good old FDs to different categories of mutual funds, you can invest as per your goals.

Mutual funds can help build a consistent income after retirement. You can invest in a combination of equity funds and debt funds in order to balance the risk and reward. That will keep you worry-free. Later, when you are ready to withdraw income, you can start a SWP (Systematic Withdrawal Plan) from your mutual funds.

Understand a 3-bucket strategy to plan for your retirement beforehand. That way, you can explore a mix of safe and growth assets to build a large corpus to retire comfortably.

Experts at VNN Wealth will help you optimize your investment portfolio for your retirement goals.

Factors to Consider Before Returning to India After Retirement

1. Your Retirement Corpus

Make sure you are on track to building your retirement corpus. When you retire, you should be able to comfortably withdraw funds.

Let’s say you are retiring in the next 5 years and will be returning to India. In this case, you can start investing in India if you haven’t already. Apart from your investments in your country of residence, your investments in India will generate wealth by the time you retire.

That way, you will be prepared to start your life in India without having to worry about moving your money.

Health insurance is very important. Evaluate health insurance plans in India to see what’s covered, and what’s not covered.

Some illnesses may have an eligibility period before you can claim them with your health insurance. If you have such illnesses, plan to buy the insurance before coming to India so that your eligibility period starts accordingly.

Make sure to see the hospital where the insurance will be accepted to avoid any surprises. Include your family in your insurance.

3. Your Stay

Where are you planning to stay once you return to India? Do you already have a home here? Or are you planning to live in a different city?

You most likely already have a home, in that case, you can easily return. Otherwise, you will have to sort your living arrangements beforehand. Buy a comfortable house as per your preferences. You can consider selling your old house and buying a new one. Make sure you won’t be in debt for long after retirement, clearing your home loan.

Consider getting a house from where the market, public transport, and a hospital are nearby.

4. Taxation

Understand your tax implications before coming to India. As NRI, you will not have to pay double tax under the Double Taxation Avoidance Agreement that India has with 70+ countries. Your income earned abroad will not be taxable in India. If you are earning any income in India, say via rent, will be taxable in India.

Once you return to India, your NRI status becomes RNOR (resident but not ordinary resident) and eventually ROR (resident and ordinary resident) over a period of a few years. You can get your taxes in line while you are RNOR. Once your status changes to ROR, you won’t be able to avail DTAA benefits.

Talk to your tax advisor before returning home so you can minimize your tax liability.

5. Professional Help to Manage Your Portfolio

Seek professional assistance in managing your investment portfolio, legal matters, and relocation logistics before returning. This will help you avoid any hurdles.

Expert financial planners can guide you with your investment in India and your country of residence. They will also help you start a monthly income from your investments after retirement. Get in touch with VNN Wealth for further information and complete guidance.

Final Thoughts

Retirement is the most awaited phase of everyone’s life. After spending years building a career and securing a financial future, you deserve a comfortable lifestyle. For most NRIs, that includes returning to India.

India is rapidly growing with a lot of potential for a secure future. You can easily build a life here with your retirement corpus built abroad. That money is worth more here in India, allowing you to afford a good and consistent lifestyle.

So, how do you want to spend your golden years? In your family home, or maybe somewhere outside the city in a cozy cottage.

Contact VNN Wealth for complete assistance in planning for your retirement.

In fact, one of the questions I’m often asked is, “How can I retire early and still enjoy a comfortable lifestyle?”

Everyone aspires to get out of their 9-to-5 grind and enjoy a peaceful life anywhere they please.

Achieving financial independence early in your life is absolutely possible. But most people I talk to seem to underestimate the importance of starting early, building the right investment strategy, and accounting for factors like inflation and healthcare.

Early retirement is achievable and sustainable with the right investment strategy and disciplined approach.

So in this blog, I will walk you through the proven strategies and necessary steps to achieve financial independence.

What does Early Retirement mean to You?

People have different goals for early retirement. Some want to retire in their 30s, others in their 40s or early 50s.

What’s your timeline? Having a clear goal in mind will help you align your investment strategies.

Secondly, define the kind of lifestyle you’d want to live after retirement. Do you want to travel a lot? Or settle in a comfortable home away from the city. What hobbies would you like to explore and can you fund those hobbies without worrying?

These are some important questions you need to ask yourself to understand what early retirement means to you.

Now, let’s unfold the retirement strategy step by step…

Calculate Your Retirement Corpus

Having a figure in mind helps build an investment approach that you can follow. Let’s figure out what amount you need to retire and live a comfortable life.

The factors you’d need to consider are:

1. Your monthly income

2. Your EMIs

3. Current corpus including your savings and investments

4. Your current age and the age at which you’d like to retire

Now let’s take an example here:

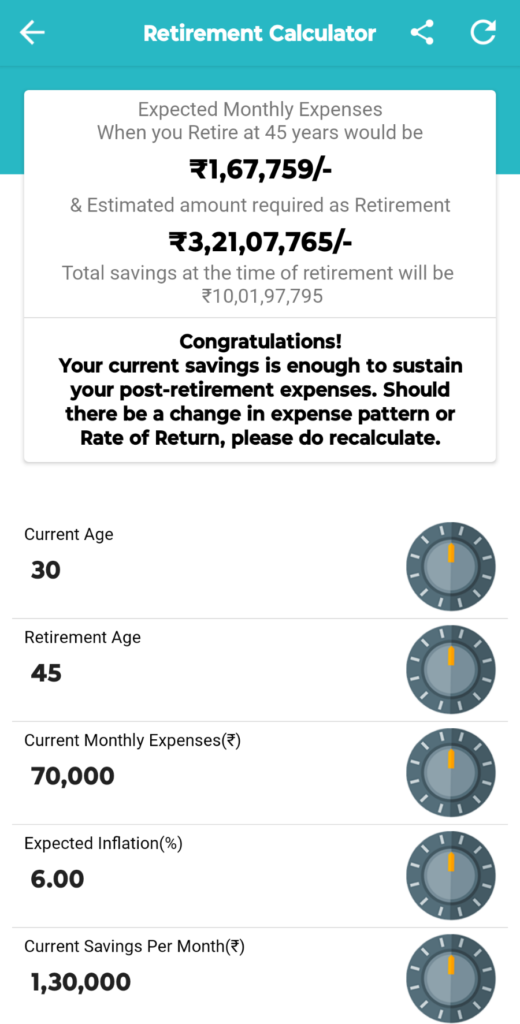

Your monthly income is INR. 2,00,000

Let’s say your monthly expense is INR. 70000. (Assuming you have closed all your loans before you retire.)

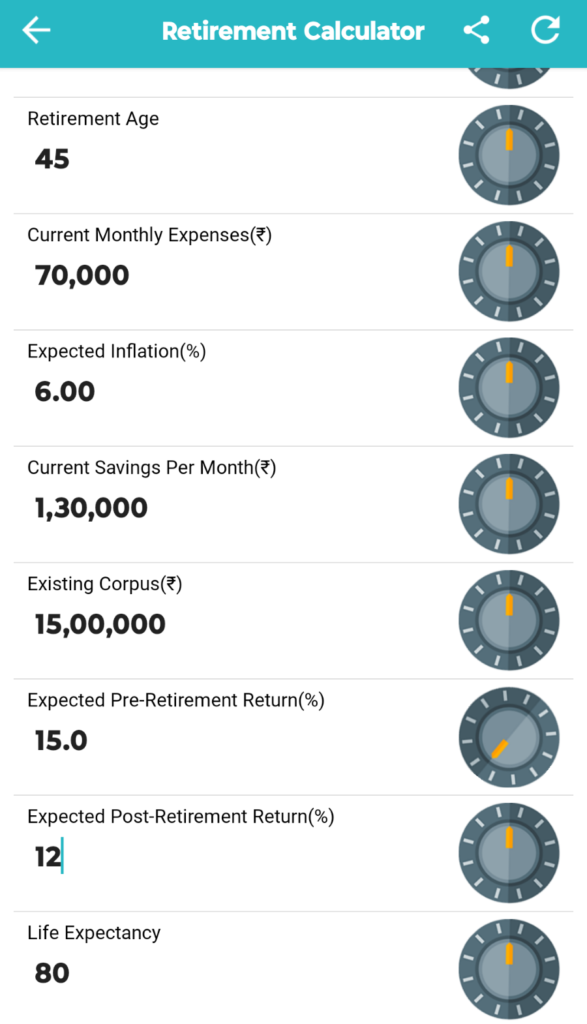

Your existing corpus including your investments is INR. 15,00,000

Let’s say your current age is 30

And the desired retirement age is 45

Additionally, you have to factor in the inflation rate, the rate of returns on your current investments, and the returns you generate post-retirement.

For the sake of calculations, let’s consider the inflation rate as 6%, the current rate of returns on your investment as 15% and the post-retirement returns to be 12%.

Based on the calculations, your expected monthly expense after retirement would be INR. 1,67,759. You’d need at least 3 crores of corpus to retire comfortably and continue the same lifestyle. And if you continue to save the same amount, you’ll be able to generate a corpus of 10cr.

Sounds promising? But it’s easier said than done.

How can you generate a retirement corpus faster to retire early?

The above example is just to show you how you can calculate your retirement corpus. However, life is unpredictable. Your income and expenses might change. Your lifestyle might change. And many external factors might influence your financial journey.

Though the numbers might change for every individual, our calculator helps you get a sense of your retirement corpus. Download the VNN Wealth app from the Playstore to explore our calculators.

Having said that, if you truly want to retire early, there are certain things you need to follow with discipline. That brings us to the most commonly followed strategy to retire early.

The FIRE Strategy: Financial Independence, Retire Early

The FIRE strategy is a philosophy centered around finance and lifestyle to help you achieve financial independence as early as possible. By following a FIRE strategy, you can retire earlier than the traditional retirement age.

The FIRE strategy encourages strategic investment, thorough financial planning, and certain lifestyle changes to achieve early retirement.

It follows a 4% rule, aka FIRE number to determine your annual expenses after retirement. The rule suggests that withdrawing 4% of your retirement portfolio every year is sustainable over 30 years.

For example, if your annual expense after retirement would be INR.10,00,000, then your fire number should be INR. 25 crores (1000000/0.04).

However, this 4% rule was created a long time ago when the economy was entirely different. It’s a historical number determined mostly by studying US trends, inflation rate, and annual rate of return.

With reference to India, the current annuity rate (average 5%) is a good reference point. That can help you generate your FIRE number.

The Core of FIRE Strategy

The FIRE Strategy stands on three important pillars.

#1. Maximizing Your Savings

To make the FIRE work, you have to save at least 50% to 70% of your income. This may sound a bit of a stretch. Most people only end up saving 15-20% of their monthly income. Realistically speaking, after all your EMIs, children’s fees, groceries, and even 30% might seem impossible.

You can try maximizing your savings by boosting your income without upgrading your lifestyle. FIRE followers often switch to a high-paying job. Or they start a side business to earn passive income.

#2. Spend Wisely

People who follow the FIRE strategy live a minimalistic life. I’m not asking you to stop spending. Some expenses are important.

However, you can identify areas where you can reduce or stop spending. For example, cancelling subscription of services you no longer use. Cooking at home instead of eating out. Not upgrading your gadgets unless they are not usable anymore. Renting a house vs buying. Tracking your monthly expenses, etc.

These small changes can help you save up to 30% more.

I have a client who retired early with a 30 crore corpus at the age of 50. He was in the merchant navy and was mindfully saving and investing throughout. His first SIP amount was monthly 1000 rupees. Over the years, as his income grew, he’d always increase his SIP amount instead of upgrading his lifestyle. Even after generating a large corpus, he spends wisely. Today if you ask him, he’ll only tell you to invest consistently instead of chasing returns.

#3. Make Smart Investments

All that money you are saving can make you more money if you invest it wisely. How and where you invest can be a game changer.

Ideally, you should start investing early to benefit from compounding. The more years you spend investing, the larger the wealth you’ll generate.

Here are a certain thing you can do to maximize your returns:

1. Understand Your Risk Appetite

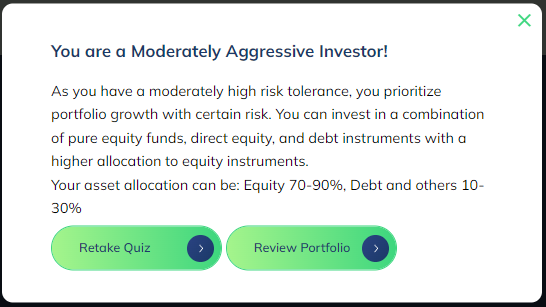

Knowing your risk appetite is crucial to optimize your investment portfolio. It helps you understand how much risk you can realistically take on your portfolio. Take a risk profiling quiz and it’ll tell you the ideal allocation across different asset classes.

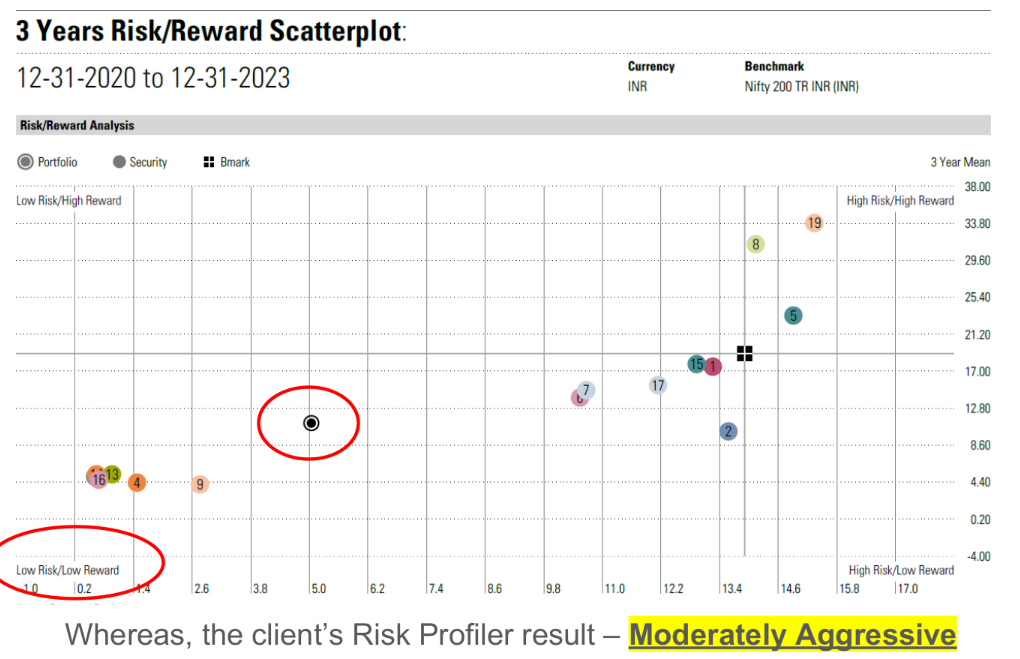

I’ll give you an example. A 55-year client reached out to me a few months ago. He said he doesn’t find mutual funds worth taking the risk as he always ends up making single-digit returns. When I reviewed his portfolio and asked him to take a risk profiling quiz. As I suspected from the beginning, he had an aggressive risk appetite but he was majorly invested in safer instruments.

Notice the black dot on the diagram. It indicates that his portfolio was inclined towards low risk/low reward, but his risk profile was moderately aggressive. I realigned his portfolio towards moderate risk and he was able to generate desired returns.

That’s why it’s important to understand how much risk you can comfortably take in order to generate desired returns.

2. Invest in Different Instruments for Diversity

As they say, don’t put all your eggs in one basket. Invest your money across equity, debt, gold, real estate, and international equity.

Invest in a combination of growth and safe assets. Growth assets can be your mutual funds, stocks, unlisted shares, etc. You can start mutual fund SIPs for a longer horizon. Safer assets can be your PPF account, FDs, and some debt funds.

Get your portfolio reviewed by an expert and create a solid investment strategy to follow. Periodically review your investments to stay on track of your goals.

3. Create an Emergency Fund and Get a Health Insurance

Emergencies can wipe out your savings without prior notice. You’ll work hard to save and invest more to retire early. But a sudden expense can derail it all.

An emergency fund is a safety net. When an emergency arises, you can survive on this fund without withdrawing your investments. Because premature withdrawals can break your investment strategy.

Set aside a certain amount that you will only use for emergencies. It should take care of your expenses for at least a year. So multiply your monthly expenses by 12 and that’s your emergency fund in case you lose your job.

Medical emergencies also tend to be expensive. Get good health insurance for you and your family. That’ll take care of your medical bills.

This way, your investments will keep growing. And you will be able to build your retirement corpus in a preferred timeline.

Types of FIRE

Even after religiously following the three pillars of the FIRE strategy, it may or may not be realistic for everyone. That’s why there are types of FIRE strategies that you can follow based on your financial situation, preferences, and goals.

Lean FIRE: Keeping your expenses lower, save aggressively to ensure your returns cover your post-retirement cost of living, and live a minimalistic lifestyle after retirement as well.

Fat FIRE: Saving and investing a ton of money, aiming for a luxurious lifestyle by building a larger portfolio.

Barista FIRE: Achieving partial financial independence and taking a part-time job to cover expenses. In Barista FIRE, you withdraw a small percentage from your retirement corpus every month and pair it with the income from your part-time job to cover your expenses.

Coast FIRE: Saving and investing wisely so your returns can cover your basic cost of living after retirement without further contributions. Here, you keep your retirement portfolio untouched and earn an income that covers your current expenses.

I have met people who are hardcore on FIRE (metaphorically) so they can retire early. They don’t allow anything that might sidetrack them from their goal. But I have also met some investors, who may not be able to completely retire early but are on a track of financial independence. You can set your own rules.

How to Stay on Track with Your Financial Goals?

1. Preparing for Market Volatility

Life is full of surprises. You have to be prepared for any hurdles you may face on your financial journey.

Market volatility, for instance, can take your investments through ups and downs. Many investors let their emotions take the front seat while making financial decisions. Emotions like fear of losses or greed can break your investment strategy.

You have to trust the process. You will only lose money if you end up making harsh decisions. So, focus on long-term perspective instead of short-term uncertainties.

Staying committed to your financial goals makes all the difference. Once you set a goal, you must try everything in your capability to achieve it. That means, having to adjust the budget during economic changes. Cutting down expenses in order to save the desired amount every month. Being a little flexible without compromising on your investments.

I highly recommend reviewing your financial plans every year to see if you are on the right track. If yes, kudos. If not, you can adjust your investments to get back on track.

3. Follow the FIRE Mindset

For any financial strategy to play out, your mindset matters a lot. If you are not emotionally invested in achieving your goals, getting sidetracked is bound to happen.

FIRE is a long-term strategy, not an overnight success. Give your investments the time they deserve to support your lifestyle post-retirement. Remember, the end goal is a worry-free comfortable lifestyle.

Ready to Retire Early?

If you’ve reached the end, that means you genuinely want to retire early. I’d say your willingness to follow a disciplined approach is a big start.

The next step is to get your portfolio reviewed and create a roadmap to follow to reach the desired destination. Experts at VNN Wealth are happy to accompany you throughout.

Get in touch and let’s plan for your early retirement!

The biggest obstacle between you and your financial goals is- You! Your emotional investing is causing more harm to your portfolio than you realize.

In an ever-changing financial landscape, it’s easy to let emotions influence your decision. You’re a human after all.

But… Your fear, greed, and overconfidence, are clouding your judgment, pushing you towards making an irrational decision.

Strong portfolios and successful investments require discipline and emotional stability. And if a small part of you feels you’ve allowed your emotions to overpower your decisions, then this blog is for you.

Keep reading as we’ll explore how emotions can impact investment and simple strategies to keep them in check.

Understanding Emotional Investing

We let our emotions control the situation in almost everything in our lives. Instead of relying on logic or data, we let our feelings make the decision for us. We do the same with investments.

Does any of the following sound familiar?

Fear: In fear of losses, you end up selling your investments during a market dip.

Greed: Taking unnecessary risk by chasing the returns during a market rally.

Overconfidence: Trying to time the market, leads to impulse decisions.

FOMO: Fear of missing out on the market trends.

Regret: Irrational decisions in the hope of covering the previous losses.

Here are some of the examples that may also sound familiar:

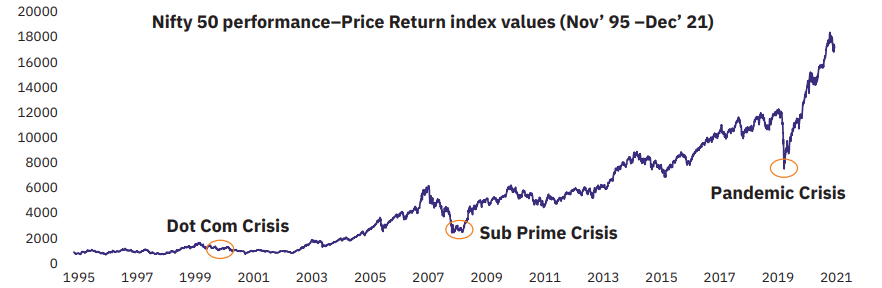

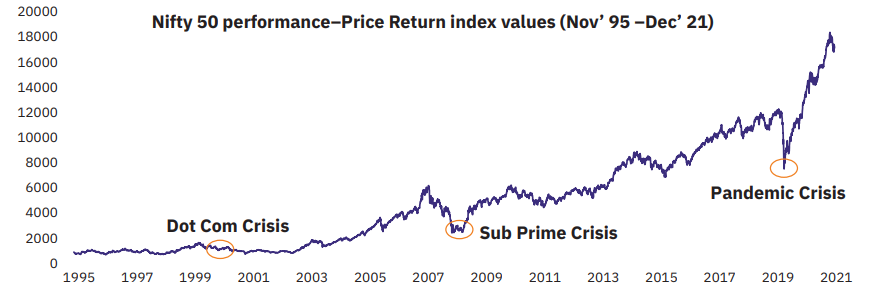

When the market crashed during COVID-19, a lot of investors cashed out their portfolios in fear of losses. However, the market rallied up soon after. The Nifty 50 went up by 124% between April 2020 to Oct 2021.

Similarly, in 2008, Sensex experienced its biggest crash in January and continued to decline for the rest of the year. Investors sold significant portions of their investments to avoid further loss. Sensex recovery took more than a year. During this crisis, patient investors survived but emotional investors caused a huge dent in their portfolio.

Market crashes are temporary and markets always eventually recover. During these tough times, your actions can make or break your portfolio.

The Psychological Traps of Emotional Investing You Should Avoid

People often let several psychological biases alter their investments. These biases arise from the need to stay in control of your money. We’ve noticed one or the other of the following psychological traps clouding the decisions of the investors we meet.

1. Herd Mentality

The most common trap that people fall into is following the crowd. From buying a car to careers and investments, people tend to follow others.

For example, during the dot-com bubble, everybody invested in tech stocks and lost significant wealth when the bubble burst in 2000.

The backbone of this herd mentality is fear of missing out. People want to jump on the bandwagon with others, follow the same path. However, what works for others may or may not work for them.

Everyone’s financial situation and investment goals are different. Therefore, as comforting as it appears, following others while investing does more harm than good.

2. Loss Aversion

Studies show that investors tend to feel the pain of losses more deeply compared to the joy of gains. The fear of losses prompts premature selling during the market dips.

We’ve met plenty of investors who, despite a defined time horizon for their investments, get restless with temporary loss.

What these investors fail to understand is, that market corrections aren’t going to last forever. As the economy grows, the markets eventually follow. Therefore, market volatility can be mitigated by time.

As you can see in the graph above, every market crash was eventually recovered. You need to be patient. Your investments deserve time to recover from the losses. Don’t let the temporary loss get in the way of your long-term growth plan.

3. Selective Thinking

People always try to make sense of their decisions by selective information. They want to believe in what they want.

For example, someone who is convinced that real estate is the best investment option will only focus on success stories. They’ll only pay attention to rising real estate prices in certain areas. Or positive experiences of their friends. Their upbringing and their family’s beliefs also play a role. These people only see what they want to see and completely overlook risks like market downturns, maintenance costs, or long periods with no rental income.

They try to seek information that aligns with their beliefs. This bias leads to misinformed decisions.

You’re trying to build wealth to make your financial future secure. You should trust relevant data to make an informed decision.

Strategies to Keep Emotions Out of Your Investments

1. Create a Well-defined Investment Plan

Disciplined investment is the key. Having clear financial goals will help you stay focused, even during market uncertainties.

Here’s what you need to do:

Step 1: Define your goals. For example, buying a car next year. Moving into a new house in two years. Or retiring early. Assign a tentative amount to each goal that you’ll need to generate.

Step 2: Evaluate your financial situation. Get all your statements and note down your monthly expenses, EMIs, funds you’re keeping for emergencies, salary increments, etc. This will help you set aside an amount you can invest every month.

Step 3: Take a risk profiling quiz to understand your investment personality on the spectrum of aggressive to conservative. Many investors like to believe (or pretend) they’re aggressive investors. However, the kind of risk you’re willing to take and the risk you can actually take is different. So answer honestly and the quiz will give you the suitable allocation of equity, debt, and other instruments. For example👇

Step 4: Evaluate your investment portfolio. Review your current holdings and realign them as per your risk profile.

2. Invest in Different Asset Classes

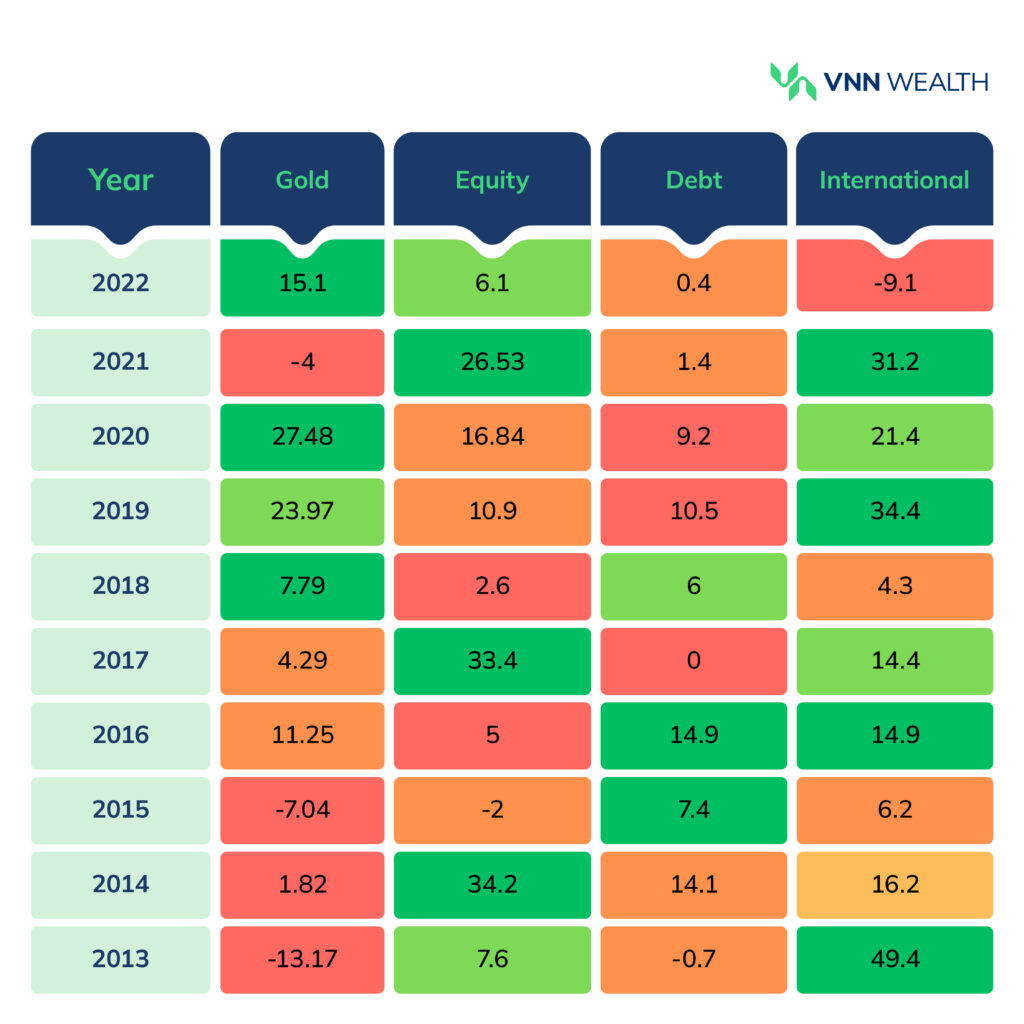

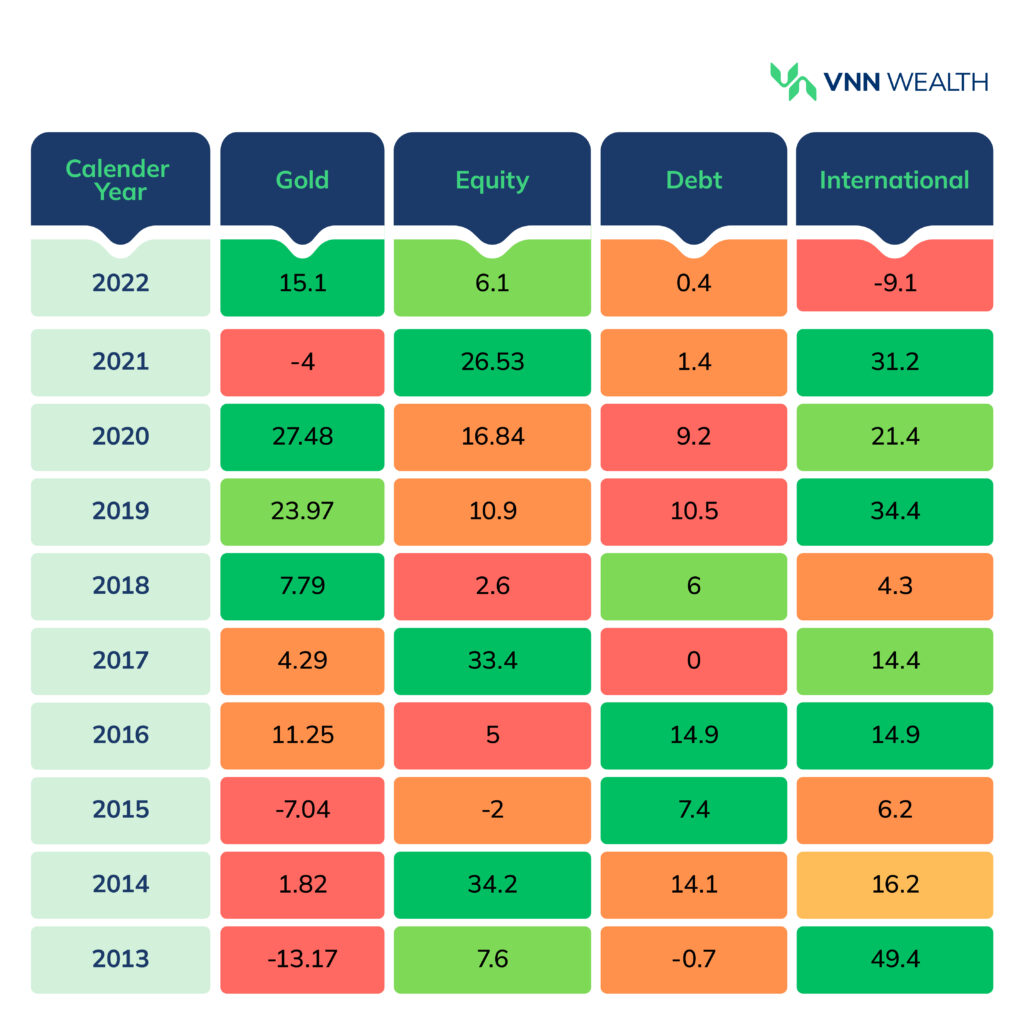

Asset allocation is crucial to maintaining a diverse portfolio and balancing risk. Equity, debt, and gold each experience a different cycle every year. However, they complement each other.

Take a look at the table below. The performance of each asset class varied every year.

So if you are worried about your portfolio crashing, don’t invest heavily in one asset class. That’ll lead to high-concentration risk. Instead, distribute your money across different instruments to balance the risk. That way, you won’t be tempted to make any impulse decisions.

3. Pay Attention to the Investment Horizon

Let’s take a simple example. Baking a cake requires a specific amount of time to cook completely. If you take it out of the oven before the timer finishes, you’ll be greeted by an undercooked cake.

Similarly, when you invest money in an instrument, it needs a specific time to deliver returns. Premature withdrawal will cause a loss.

So, when you define goals, you must assign a timeline for each. For example, buying a house in two years.

Since your time horizon is only two years, investing in small-cap or mid-cap funds would be silly. These funds need 5+ years to deliver optimal returns. Instead, you can invest in debt funds with a suitable horizon. On the other hand, your time horizon would be longer to achieve your retirement goals. In that case, you should definitely invest in high-risk funds.

Because…risk is not defined by a fund category but by a time horizon. Each mutual fund category has a pre-defined time to mitigate short-term volatility.

Goal

Timeline

Mutual Fund Category

Buying a car

Within 3 to 6 months

Low-Duration Debt Funds such as: Kotak Low Duration Fund Axis Treasury Advantage Fund SBI Magnum Low Duration Fund

Moving into a new house

In 3 years

Dynamic Bond Funds / Banking and PSU Funds / Hybrid Funds like Balanced Advantage Funds, Multi-Asset Funds: ICICI Prudential Balanced Advantage Fund Kotak Balanced Advantage Fund Quant Multi Asset Fund

Wedding

In 3 to 5 years

Large Cap Funds such as: Nippon India Large Cap Fund ICICI Prudential Bluechip Fund SBI Bluechip Fund

Children’s Education

Within 5 to 7 years

Mid Cap Funds such as: Quant Midcap Fund Motilal Oswal Midcap Fund HDFC Midcap Opportunities Fund

Retirement Planning

7 Years and Above

Small Cap Funds such as: Nippon India Small Cap Fund Quant Small Cap Fund TATA small cap Fund

Important: The above table only illustrates time-based investments. However, you also need to consider other parameters such as your risk appetite, the fund’s rolling returns (consistency), and your overall investment portfolio. Choose funds that align with your objectives and contribute to the growth of your overall portfolio.

4. Automate Your Investments

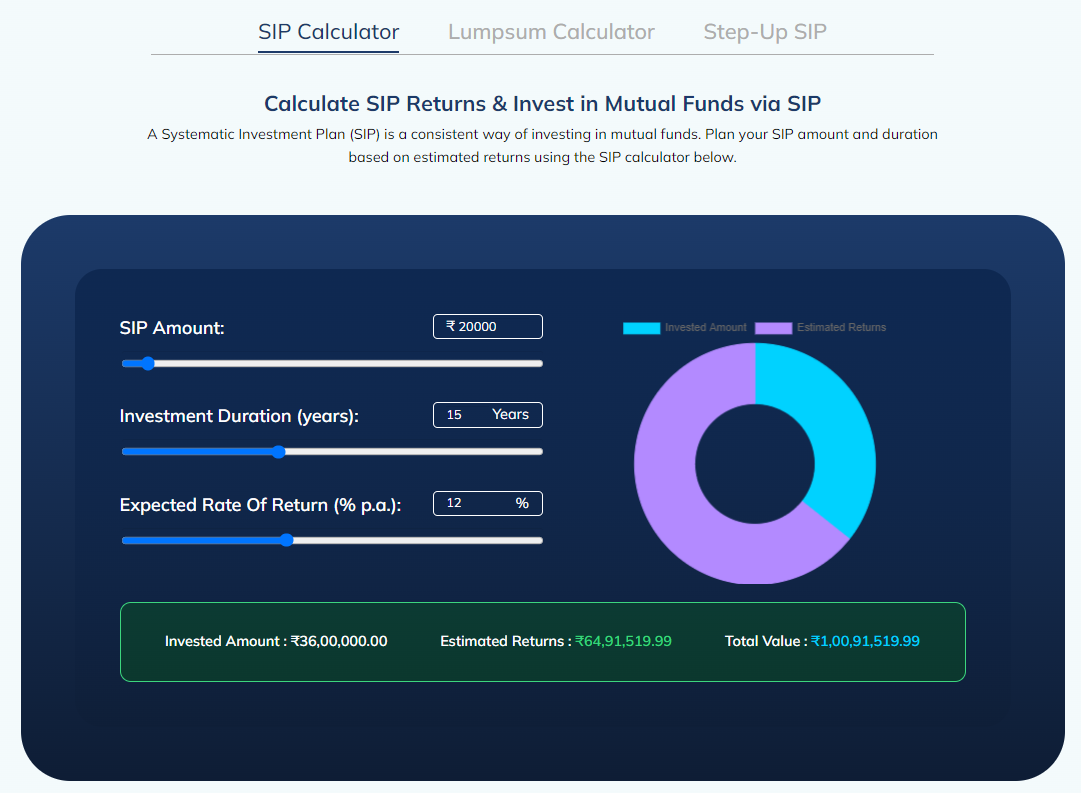

Automation removes the temptation of timing the market. It helps you consistently invest toward your goals. You can set up an SIP (Systematic Investment Plan) for mutual funds of your choice.

Here’s how disciplined consistent investment can compound over a period of time. Let’s say you aim to accumulate 1 crore for your child’s college education over the next 15 years. By consistently investing INR 20,000 per month in mutual funds, with an expected average annual return of 12%, you can reach this financial goal within 15 years.

You can play around with numbers using our SIP calculator to set a specific timeline for your financial goals. Automate your SIP installments and let the money compound on its own.

5. Seek Professional Advice

A professional financial expert will objectively evaluate your investments. They will provide data-driven insights to strengthen your portfolio irrespective of the market conditions.

A professional financial expert can:

Analyze your risk appetite and review your portfolio.

Assist you in choosing the right mutual funds.

Ensure your portfolio’s risk aligns with your risk profile.

Help you identify redundant investments and ensure true diversification.

Guide you through the market volatility.

So, even if you’re a savvy investor with market knowledge, an expert can shed light on the situation from a different angle.

Emotional Investor Rahul often gets anxious about market uncertainties. He constantly monitors his portfolio and complains about poor returns. He ended up investing in multiple stocks due to a trend his friend was following and sold it at a loss when the stock price began declining. His patience runs out after every minor change in the market and he starts panic selling or impulse purchasing. He claims to be an aggressive investor but never bothers evaluating his actual risk appetite.

In contrast, Pratiksha, a Rational Investor always focuses on a long-term picture. She invested in various asset classes for diversification and follows a strategy based on her risk appetite. While her portfolio also goes through ups and downs, she is not concerned. She keeps investing via SIP for a defined horizon and lets the money compound. She quarterly monitors her investments only to see where it is going and talks to an expert if she has any questions.

Outcome? Pratiksha’s consistency and data-driven approach will outperform Rahul’s emotional investing. While Rahul might make quick gains sometimes, these wins are unpredictable.

Therefore, always stick to an investment strategy catering to both short-term and long-term goals.

How to Recover from Emotional Investing Mistakes?

Acknowledge your mistake: Start by accepting your mistake. Identify the situations where you let your emotions run wild. Moving forward, you can stop yourself from making the same mistake again.

Re-evaluate your portfolio: It’s never too late to fix any errors. Re-evaluate your portfolio with an expert- identify gaps, poor-performing assets, redundant investments, etc. Sell the assets that are consistently delivering poor returns. Reallocate your money to asset classes that’ll deliver returns ideal for your financial goals.

Focus on consistency: Encourage yourself to focus on disciplined investment. Plan Systematic Investments via SIPs or STPs. That way, you will invest a small amount every month and benefit from compounding.

Keep your emotions in check: If you feel stressed about your investments, try to have a long-term perspective. Some stress management techniques such as meditation, exercise, or hobbies can help you navigate your emotions. It’s easy to worry when the market is fluctuating. But, focus on what you’re trying to achieve with your investment so you won’t get side-tracked.

Conclusion

Emotional investing can be detrimental to your long-term financial success. Fear, greed, ego, overconfidence- all these emotions push you in the wrong direction. Instead, unlock your emotional intelligence to make logical, goal-oriented investment decisions.

As Daniel Kahneman says in his book Thinking, Fast and Slow- emotional decisions can be impulsive whereas rational decisions require more thought.

So, this is your sign to rethink your financial decisions. Make the right choice by creating a strategy for better returns. Have a long-term perspective than a short-term panic. Start making small changes today and you’ll notice the results in due time.

Ready to Invest?

Are you ready to give your investment portfolio another chance?

3: Sign up or log in to start investing. Effortlessly automate your SIPs and STPs.

If you’re interested in exploring wider investment instruments such as unlisted shares, AIFs, and PMS, reach out to us. VNN Wealth is a trusted wealth management firm in Pune with exclusive investment opportunities tailored to your financial objectives.

Retirement is the golden era of your life. You finally relax. Sit back in your rocking chair with a cup of tea. You have time for your family and most importantly, for yourself.

However, the ride through the retirement years will only be smooth if you plan for it beforehand.

Currently in India-

Only 10% of the 60+ population is earning from the pension or the rent.

About 60% of men and 25% of women above 60 are still working.

And 60% of the people above the age of 70 are dependants.

Planning for retirement is one of the crucial pillars of your financial journey. You spend years working hard and building wealth. That wealth should keep you afloat for the rest of your life.

So here’s how to ensure you never run out of your retirement corpus. While this blog is designed for someone nearing retirement, young investors can also learn and plan beforehand.

Know What You Want

Let’s take an example- When you visit a retail store to buy a TV, you likely have certain specifications in mind. You tell the salesperson those specifications, and they suggest options that meet your needs. But, if you’re unsure about what you’re looking for, the salesperson might try to sell you a TV on which he earns more commission.

Similarly, if you don’t know what you want for your retirement, you won’t be able to create a proper plan. Your bank RM might push a ULIP or some insurance plan that sounds good but may or may not align with your financial needs.

Therefore, it is crucial to know what you want. And how do you do that? Read along to find out everything you need to know about retirement planning.

1. Set Clear Goals

How do you want to spend your retirement? Maybe in a cozy cottage away from city life. Or annual international trips with your spouse. Everything is possible by aligning your portfolio to fulfill your goals.

But the primary step is to set a goal for your income expectations. There are multiple ways to draw a consistent income after retirement.

1. Rental income from your residential/commercial property.

2. Monthly withdrawals via systematic withdrawal plan (SWP) from your mutual funds.

3. Annuities

If you’re salaried, you might also receive a corpus built in your PF after retirement. You can strategically invest it to draw monthly income. Talk about your goals to your financial advisor. Discuss the required corpus to live a life you want to live.

At what age you’d want to retire? What would be the timeline for your goals set for post-retirement life? Give it all a thought. Talk to your spouse and children to accommodate them into your goals. That way, you can choose the investment instruments catering to specific objectives.

Here are the mutual fund categories that you can choose based on the horizon:

Time Horizon

Fund Category

0-3 Years

Debt fund/hybrid fund

3 to 5 Years

Large Cap Funds

5 to 7 Years

Mid Cap Funds

7+ Years

Small Cap Funds

3. Assess Your Risk Appetite

Your overall risk profile is an important factor in retirement planning. It involves analyzing your financial situation to decide how much risk you can take.

Nine out of ten times, people ignore their risk appetite. They just invest, only to find out the returns on their portfolio do not live up to their expectations. Either the portfolio is delivering low returns when a person can take higher risk. Or the portfolio is full of aggressive investments when a person has a low to moderate risk appetite.

Don’t let that happen to you. Take a risk profiling quiz to know where you stand. Answer honestly to receive insights on the asset mix that fits your profile.

4. Review Your Existing Portfolio

Your financial goals and risk appetite constantly keep evolving. Your initial investment strategy will not work for your retirement plan. Now you need a completely different strategy, which can be built against your existing portfolio.

Review your existing investment with a financial advisor. They’ll identify the gaps in your portfolio and realign it with suitable asset allocation.

5. Have an Opinion About the Market

This step is not mandatory, but it’s always good to be aware.

The market moves in a similar direction as the economy in the long run, with occasional fluctuations. So if you’re paying attention to the news about the global economy and its impact on Indian markets, you can easily form an opinion. The market awareness, at least to some extent, will help you choose the right instruments. It’ll also help you better understand your financial advisor’s suggestions to make an informed decision.

Here’s an example of how having a market opinion can help you choose the right funds:

When the markets are uncertain, your focus should be on asset allocation. You can invest in hybrid funds such as Balanced Advantage Funds, Flexi Cap Funds, or Multi Asset Funds for diversification.

Each fund has a different asset allocation and a cash component to rebalance the allocation based on market scenarios. Fund houses use an inbuilt model based on various parameters for rebalancing.

1. If you think the markets are expensive at the moment and may decline: Choose balanced advantage funds with more cash holdings as these funds can buy more equity when the market declines.

2. If you think the markets will rally further, choose balanced advantage funds with more equity holding to capitalize on growth.

3. If you don’t have any opinion, choose multi-asset funds to get instant diversification across equity, debt, and gold.

Similarly, a market outlook across small-cap, mid-cap, and large-cap will help you decide which flexi-cap fund to invest in. Flexi cap funds offer allocation across market cap based on the market conditions.

5 Things to Consider While Planning For Retirement

1. Emergency Fund

Emergencies never announce themselves. A sudden expense may dent your financial plan. It’s always better to be prepared for such scenarios. Build a highly liquid emergency fund that you can withdraw whenever needed.

Make sure you have enough saved up to cover 6-12 months of your expenses. Instead of keeping these funds in your savings account, park them in liquid funds. Liquid funds offer a 1-2% extra interest rate compared to the savings account.

Buy a health insurance plan for yourself and your family. It’ll take care of your medical emergencies without draining your savings.

2. Inflation

Inflation is inevitable. Today’s INR 50,000 monthly expense would be INR 1,60,000 after 20 years with a 6% inflation rate. You will need more money to continue or upgrade your lifestyle after retirement. You can’t avoid inflation but you can certainly surpass it by optimizing your portfolio.

3. Cash Flow

While planning retirement, keep your short, medium, and long-term goals in mind. Goals are essentially your expenses. Let’s say your monthly expenses after retirement are INR 2,00,000. To plan expenses for the next 3 years, you’ll need INR 7,200,000 kept in liquid assets for easy withdrawals. The rest of your retirement corpus can be invested as per your expenses in the next 5 to 6 years or even longer as per your financial plan.

4. Estate Planning

Transferring legacy to successors is still quite common in India. If you are planning to hand over your assets to your children, you may want to plan your finances accordingly. Consider your monthly expenses and the cash flow to have a comfortable life for yourself. What’s left after that can be invested in various assets for your children to inherit later.

In order to seamlessly transfer your legacy, you must create an estate plan. Drafting a will or creating a trust avoids family disputes. It ensures the transfer of your assets as per your wishes, thereby financially securing your loved ones.

5. Taxation

Last but not least, the taxes. You have to pay tax on gains and income generated through your investments. Similar to inflation, taxes are unavoidable. However, you can dodge some taxes by optimizing a tax-efficient exit strategy. Your financial advisor will assist you with an exit strategy that ensures better post-tax returns on your portfolio.

If you don’t have a financial advisor, get in touch with VNN Wealth. Our experts will help you plan for your retirement.

Now that we’ve covered all the basics, let’s discuss the most commonly followed retirement planning strategy.

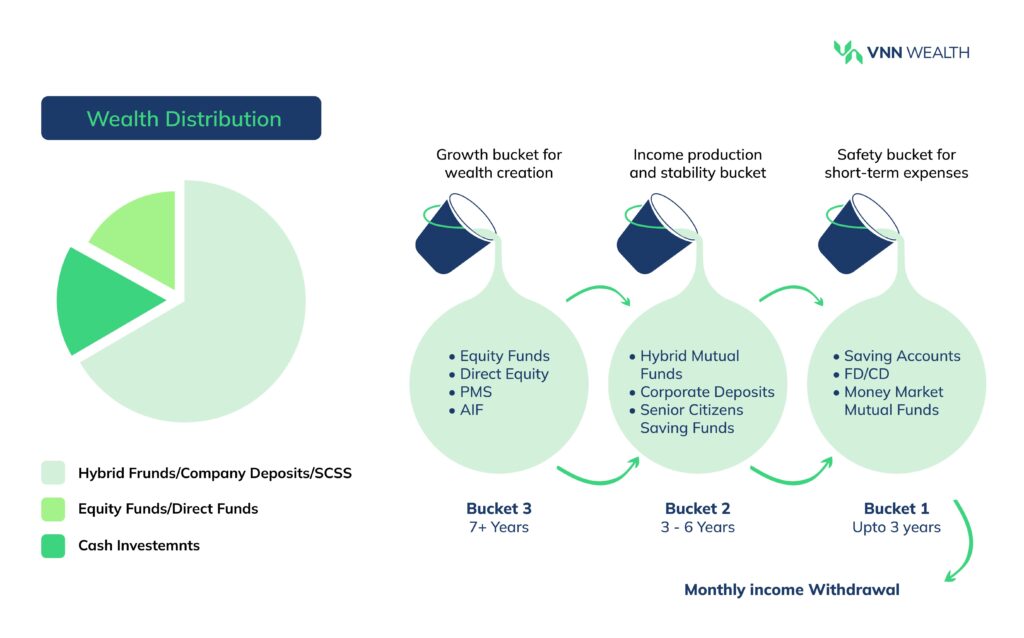

The 3-Bucket Strategy For Effective Retirement Planning

This is the most commonly followed strategy to manage your retirement corpus. The 3 buckets represent your financial needs for a particular period. Together, these buckets keep your funds moving, thereby offering you financial freedom.

Bucket #1: Short-Term Financial Goals (1 to 3 Years)

The 1st bucket, AKA Safety Bucket, contains highly liquid assets to cover living expenses for up to 3 years.

Let’s assume for the sake of example that your monthly expense after retirement would be INR 2,00,000. In that case, you can fill bucket 1 with INR 7,200,000 to comfortably cover 3 years of expenses.

Those INR 7,200,000 can be invested in high-liquidity instruments.

1. The most common liquid and safe instruments are Fixed Deposits, Certificates of Deposits, or Liquid Funds.

2. Money Market mutual funds can also be included in this bucket. These funds invest in highly liquid assets.

3. While many prefer keeping funds in savings accounts for emergencies, you can also consider short-term debt funds.

Debt funds offer liquidity, better yield than savings accounts, and are available in variable time horizons.

As of May 2024

This bucket offers financial safety even during market downturns and avoids the need to sell long-term investments.

Bucket #2: Medium-Term Financial Goals (3 to 6 years)

Bucket 2 is a Stability Bucket for medium-term goals. The assets in this bucket cater to 3 to 5 years of financial needs.

While you are emptying the 1st bucket, investments in bucket 2 can generate interest to refill the 1st bucket.

1. Fill the second bucket with Corporate Fixed Deposits, Hybrid Mutual Funds, and Senior Citizen Saving Funds.

2. Corporate FDs are slightly riskier than bank FDs but offer superior interest rates. That extra 1 to 2% can make a huge difference.

3. Hybrid Mutual Funds invest in equity, debt, and gold. For example- Balanced Advantage Funds, Multi Asset Funds. These funds are less riskier than pure equity funds and are suitable for intermediate financial goals.

4. Senior Citizen Savings Scheme can also be a part of a medium-term financial plan. Retirees can invest INR 1,50,000 in a financial year to get an exemption on tax under section 80C of the IT Act.

The second bucket aims towards income production and stability with less volatile investments.

Bucket #3: Long-Term Financial Goals (7+ Years)

Bucket 3 is the growth bucket for wealth creation. While the first two buckets are taking care of your expenses, the 3rd bucket can keep generating more wealth. You can keep it untouched, or use the gains/capital to refill the previous two buckets.

1. The best instruments to fill this bucket with are equity mutual funds, direct equity, and alternative investment funds (AIF). These instruments are capable of delivering superior returns in a longer horizon.

Final Thoughts: How to Divide Your Retirement Corpus Into 3 Buckets?

Diving your retirement corpus into 3 buckets depends on your overall portfolio, expenses, goals, preferred investment horizon, and the income you want to generate post-retirement.

There’s no one-formula-fits-all. It’ll change as per your financial requirements and goals. The idea is to keep the cash flowing through the buckets.

If you want to manage your retirement corpus, experts at VNN Wealth will help you create a personalized 3-bucket strategy. Get your portfolio reviewed by our experts and optimize your portfolio to plan for a stress-free retirement.

Picture this: You’re sipping a warm cup of coffee with your loved ones, knowing that a steady stream of income is flowing into your bank account. Even better if you don’t have to work for it.

This vision of financial independence is achievable through smart investments. You can generate a steady stream of income for your retirement or simply have passive income for your family.

Two of the popular options investors explore to generate regular income are:

1. Real estate investments for rental income 2. Income from mutual funds via systematic withdrawal plan (SWP)

In this blog, we will discuss both these options in more detail, exploring how they work, how much initial investment is required, and what their advantages and drawbacks are.

Generating Income Through Real Estate

Real estate investment involves purchasing a residential or commercial property. As it’s a tangible asset, you own it in a physical form.

In order to generate consistent income from it, you ideally have to rent out your property with a long-term lease agreement.

The rental income depends upon many factors such as rental yield in the area, property’s condition, and market demand.

Generating Income Through Mutual Funds

Mutual funds are a collection of stocks, bonds, gold, and international equity. You can invest in mutual funds that align with your risk appetite and financial goals.

The ideal way to generate income from mutual funds is to invest for a long horizon, let the money compound, and then start a systematic withdrawal plan. A Systematic Withdrawal Plan (SWP) allows you to set an amount and frequency at which you’d like to receive income. The fund units worth the amount you’ve chosen will be sold and the amount will be transferred to your savings account.

Now, we will compare real estate vs mutual funds for monthly income against various parameters.

Real Estate vs Mutual Funds for Monthly Income: Detailed Comparison

Let’s take an example: Vikas wants to generate INR. 50,000 monthly income. He’s exploring both the options- rental income and SWP. Let’s help him figure out what makes more sense…

1. Initial Capital Requirement

Real Estate

Your initial investment will vary based on the location, type of real estate property, size, amenities, etc. The rental income depends upon the rental yield in the area. In India, the residential rental yield ranges from 2 to 4%. Here’s a snapshot of the rental yield in different cities in India.

City

Rental Yield

Delhi NCR

2.79%

Bangalore

3.45%

Mumbai

2.44%

Ahmedabad

3.22%

Chennai

3.10%

Hyderabad

3.16%

Pune

3.09%

Kolkata

3.96%

Let’s take 3% for the sake of understanding.

For Vikas to generate an income of INR 50,000 from residential real estate, he’ll have to purchase a house worth 2 crores.

Property value = Annual rental income (50000 x 12) / rental yield (0.03- converted into decimal) = 600000/0.03= 2 crores

Now let’s say Vikas pays a 20% downpayment, which is 40 lakhs, he’ll have to take a home loan for the remaining amount i.e. 1.6 crores.

With an 8% home loan rate and 20 years of tenure, his EMI becomes 1,33,830. Even if he generates a rental income of INR 50,000, he will still have an expense of INR. 83,830.

On top of that, Vikas will have to pay the cost of home ownership. Brokerage (1-2% of the total value), stamp duty (4-7%), registration fee (1%), parking space (~10k/month), maintenance charges (varies as per location and amenities), etc.

Mutual Funds

On the flip side, Vikas will only have to invest 50 lakhs in mutual funds to generate INR. 50,000 monthly income.

Mutual funds deliver superior returns compared to real estate. For the sake of calculations, it’s better to be conservative. So we’ll take 12% p.a. as the average return on your mutual fund investment over a longer horizon.

Investment amount = Annual income (50,000 x 12= 6 lakhs) / 0.12= 50 lakhs

The same income can be drawn from mutual funds via SWP by investing only 50 lakhs instead of 2 crores. Plus, while you withdraw monthly 50K, your remaining amount keeps compounding, so you can keep withdrawing 50K/month for the next 20 years, at least.

With mutual funds, Vikas has an option to invest a small amount via SIP to gradually build his wealth.

Monthly SIP Amount

Average Return p.a.

Investment Horizon

Wealth Accumulated

20,000

12%

20 years

1,99,82,958

Total Wealth Accumulated in Mutual Funds

Average Return p.a.

Monthly Regular Income via SWP

Years of Regular Income

1,99,82,958

12%

1,00,000

20

This example is only for the sake of understanding. Parameters like initial investment amount, investment horizon, and average rate of return may change the calculations.

2. Risk and Return Profile

Real Estate

Real estate investment is usually less risky than mutual funds. Market fluctuations have little impact on real estate. However, you may also face a risk of vacancy, tenant default, holdover tenancy, legal disputes, maintenance issues, etc. Additionally, there’s a chance of depreciation in property value during the economic slowdown.

Real estate delivers potential returns from rental income and property value appreciation. You can expect about 8% to 10% p.a. average return on real estate investment in 10 years. It varies depending on the city, property conditions, economic conditions, etc.

Mutual Funds

Mutual funds have a certain risk associated with them based on the category and market movements. You can invest in mutual funds based on your risk appetite and financial objectives. Take our risk profiling quiz to understand the equity and debt exposure suitable for you.

The return on your mutual fund portfolio depends upon the type of scheme, investment horizon, market conditions, etc. Mutual funds deliver superior returns in a longer horizon despite market volatility. You can expect 12% p.a. average returns in 10 years. You can even generate 2% to 5% returns over and above average if you periodically review your portfolio and optimize it to generate benchmark-beating returns.

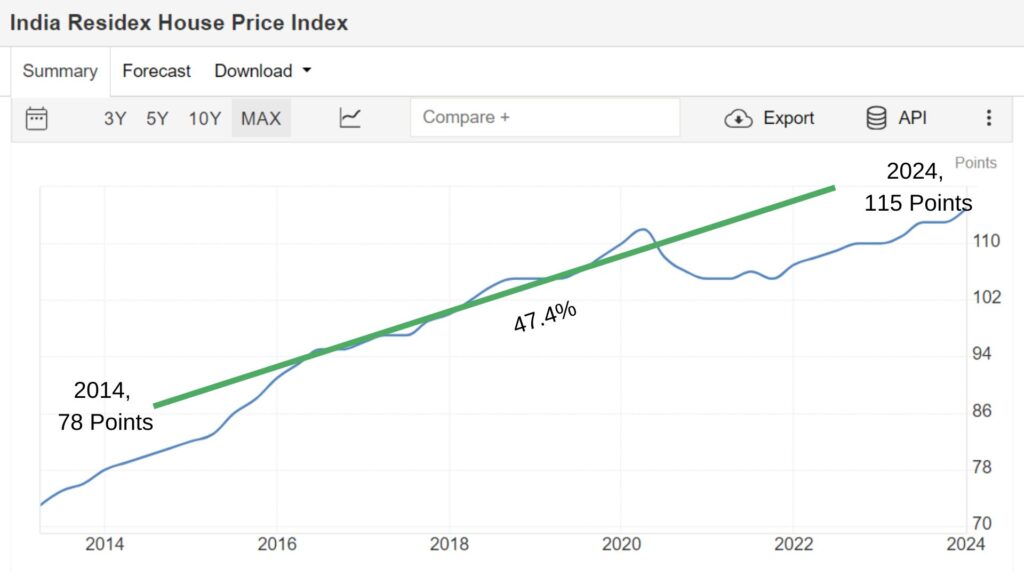

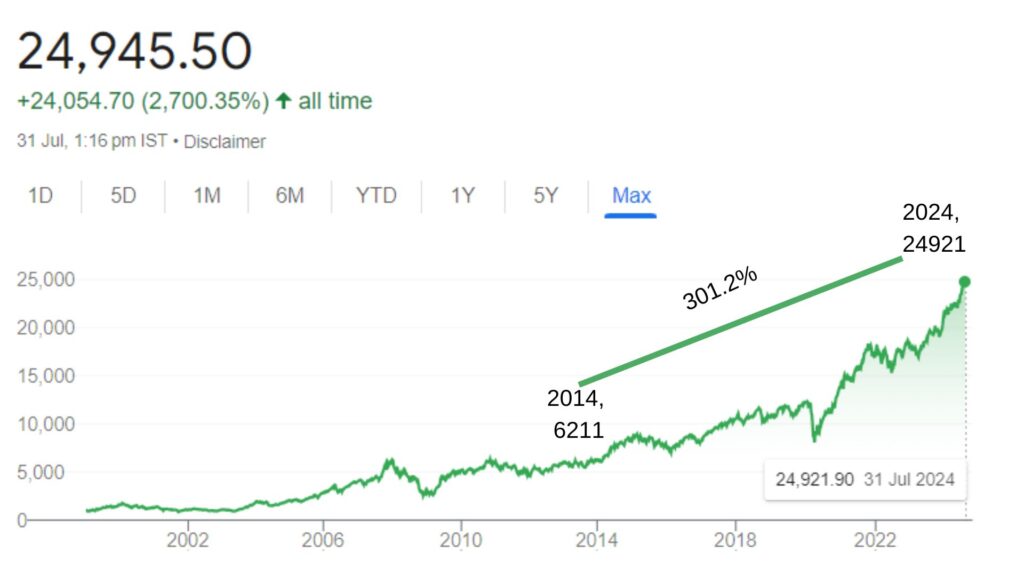

India Residex House Price Index vs Nifty 50 (2014 to 2024)

Residex has grown by 47.4% between 2014 to 2024, whereas Nifty has grown by 301.2%. Evidently, you’ll make better returns from mutual funds compared to real estate.

3. Liquidity and Accessibility

Real Estate

Real estate investments are less liquid compared to mutual funds. The property sale takes a lot of time. You’ll have to go through the hassle of property transfer paperwork and the cost associated with it. Plus, you may not get the price that you’re looking for. It’s not as easy as redeeming mutual fund units. You have to go out, sit through the negotiations, and handle the transactions.

Additionally, you have to spend a lot of time finding a good property. It requires evaluating the location in person before making a decision. It’s not easily accessible. So if you ever need funds for an emergency, real estate is not reliable.

Mutual Funds

Mutual funds are highly liquid and accessible online. You can invest and withdraw anytime you want. There’s no lock-in period except for ELSS mutual funds which carry a 3-year lock-in period for the purpose of tax-saving.

Otherwise, you have all the freedom and flexibility to decide the time and amount of investment/withdrawal. When you plan to start an SWP to withdraw income from mutual funds, you can automate the withdrawal amount, frequency, and date. The funds will start flowing into your bank account as per your preferences.

Plus, partial withdrawal is possible in the case of mutual funds which is not an option in real estate. In case of emergencies, you can sell some units of mutual funds, whereas, you cannot sell half your house.

4. Management and Maintenance

Real Estate

Managing and maintaining real estate property requires a lot of your attention. It’s a never-ending loop of ensuring the property is clean and functional. Following up with tenants and making sure they’re following society’s regulations. In some cases, tenants may not leave the property, causing a dispute. Be it residential or commercial, real estate investments demand your time and attention at all times.

Mutual Funds

Apart from periodic monitoring, you don’t have to look into managing your funds. Mutual fund houses have dedicated fund managers who are experts in handling all the transactions. Fund managers make decisions on the stocks to include in a scheme to leverage market opportunities. All you have to do is invest and let your money compound over the years. Once you achieve your financial goal, you can start/stop SWP anytime as per your income requirements.

5. Inflation Protection

The inflation rate in India is around 6 to 7%. The rate of inflation affects your effective return on investment.

Considering the above data:

Avg Return p.a.

Inflation

Effective Return

Real Estate

8 to 10%

6%

2 to 4%

Mutual Funds

12 to 15%

6%

6 to 9%

In the case of rental income, you can increase the rent by 5 to 8% every year. However, your post-tax returns taking inflation into account cannot beat mutual funds. Mutual funds have the potential to deliver benchmark-beating, inflation-beating returns.

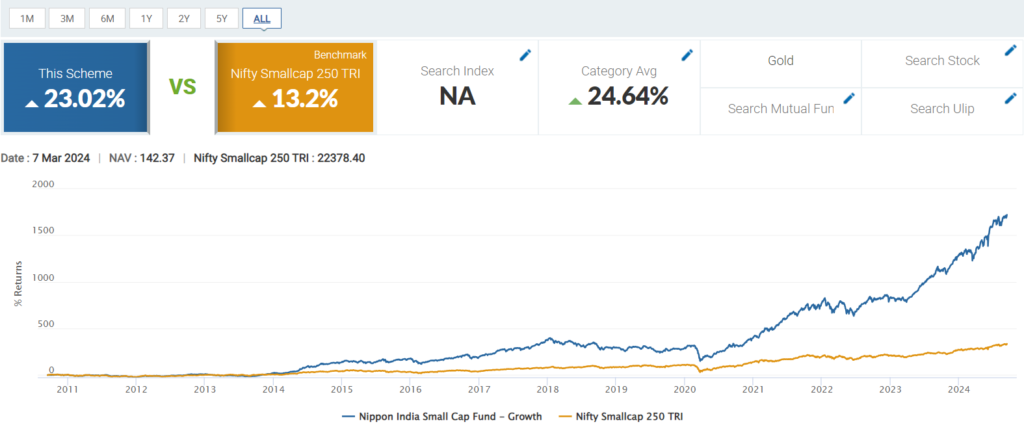

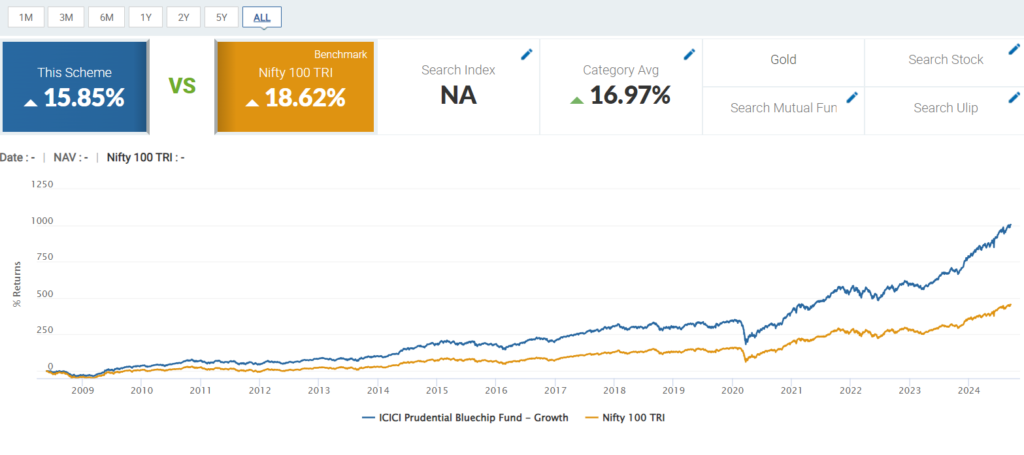

Here are some examples of funds from three different categories outperforming the index:

Nippon India Small Cap 10Y Return Against Nifty Smallcap 250

Fund NAV

Index Closing Value

10 Jan 2014

12.22

6278.90

12 Jan 2024

141.13

20906.40

Growth

1055.4%

232.9%

CAGR

28.4%

12.8%

ICICI Prudential Bluechip Fund 10Y Return Against Nifty 100

Fund NAV

Index Closing Value

15 Jan 2014

20.52

6171.25

15 Jan 2024

98.83

21508.85

Growth

381.7%

248.4%

CAGR

17.2%

13.2%

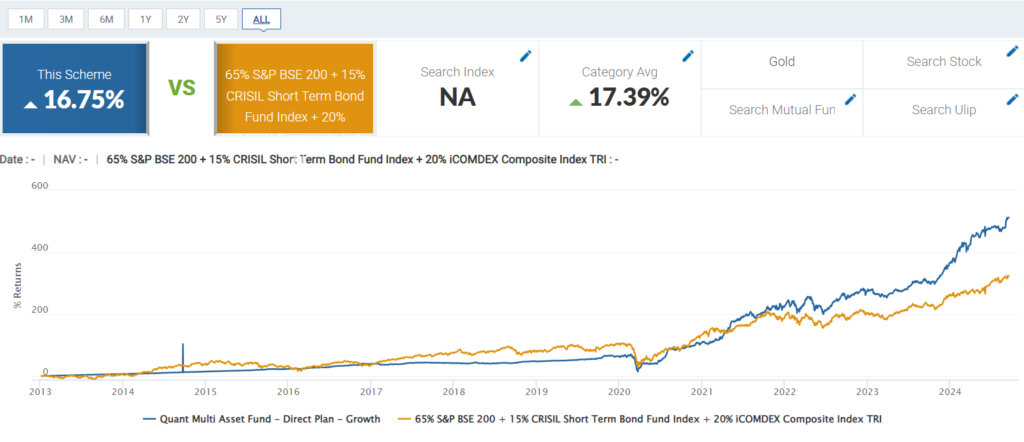

Quant Multi Asset Fund 10Y Return Against S&P BSE 200 & Short Term Bond Fund Index & iCOMDEX Composite Index

Fund NAV

Index Closing Value

16 Jan 2014

20.05

6241.85

15 Jan 2024

117.55

21441.35

Growth

486.4%

243.5%

CAGR

19.4%

13.0%

As you can see, these funds have beat their respective benchmark. The chances of earning more than the average returns are possible with mutual funds.

6. Tax Implications and Exemptions

Real Estate

1. Rental income is taxed as per the investor’s tax slab.

2. If you sell your property after 24 months, you will have to pay long-term capital gain tax. As per budget 2024, you can either opt for old taxation or new taxation, whichever attracts lower tax for you. As per the old tax rule, the long-term capital gains will attract a 20% tax with an indexation benefit. The new tax rule does not offer an indexation tax rule but the long-term gains will be taxed at 12.5%. You can get an exemption on capital gain tax by investing in 54EC bonds within 6 months of property sale/transfer.

3. You can claim an exemption on interest paid on a home loan up to a maximum of 2 lakhs under section 24. In the case of a let-out property, you can claim an exemption against the entire interest paid.

Mutual Funds

For equity-oriented mutual funds: Short term capital gain tax of 20% will be applicable on funds withdrawn within 12 months of investment. Long-term capital gain tax of 12.5% above 1.25 lakhs will be applicable on funds withdrawn after 12 months.

For debt-oriented funds Both short and long-term capital gains will be taxed as per the investor’s tax slab. You can claim exemption against ELSS mutual fund investment of up to 1.5 lakhs under section 80C of the IT Act.

Real Estate vs Mutual Funds: Quick Snapshot

Real Estate

Mutual Funds

Asset type

Tangible. Physical property.

Intangible. Units of mutual funds that are a combination of stocks and bonds.

Initial Investment Amount

Higher

Lower

Return on Investment

Rental income, price appreciation Average 8 to 10% p.a.

Capital gains and dividends. Average 12 to 15% p.a.

Liquidity

Low

High

Risk

Market slowdown, tenant default, legal disputes, maintenance, vacancy issues, etc.

Market performance

Management and Maintainance

High and costly

Professional management by fund houses. Low maintenance.

Which Option Should One Choose for Monthly Income: Real Estate or Mutual Fund?

Real estate has always been a popular investment option in India. Even today if you ask your parents or grandparents, they’ll advise you to invest in real estate. Their advice comes from an era when mutual funds weren’t regulated. The UTI mastershare fraud had broken people’s trust in mutual funds. Therefore, they preferred physical assets such as gold, real estate, cash savings, etc. Plus there’s a sentimental value attached to buying a property, mostly because it seems safer. You own a tangible property and control everything around it. And sure, if you’re insistent on buying a home to secure your family’s future, to have a place to call your own, you can definitely consider buying one.

But for the sake of generating income, mutual funds are better suited. Now SEBI regulates mutual funds to ensure investors’ money is safeguarded. You can invest as per your risk appetite, decide the amount and frequency, and let the fund managers handle the fund’s growth while your money compounds.

The clear winner here is the systematic withdrawal plan.

Conclusion

Investors often consider purchasing property to generate passive income without assessing their overall portfolio. However, mutual funds are clearly more feasible to generate regular income. The initial capital required to invest in mutual funds is significantly lower than in real estate. Plus, the cost of home ownership, the time and energy required to maintain the property, the slow growth, and low liquidity make real estate less appealing.

Mutual funds are highly liquid. You can start investing a small amount by SIP and accumulate wealth over the years. When you’re ready to withdraw income, you can easily set up an SWP online. Unlike real estate, mutual funds have the potential to deliver benchmark-beating, inflation-beating returns if you truly diversify your portfolio and periodically optimize it.

Ready to Generate Regular Income?

Take a risk profiling quiz and review your portfolio today. Learn more about the Systematic withdrawal plan from our experts and revamp your portfolio to generate monthly income.