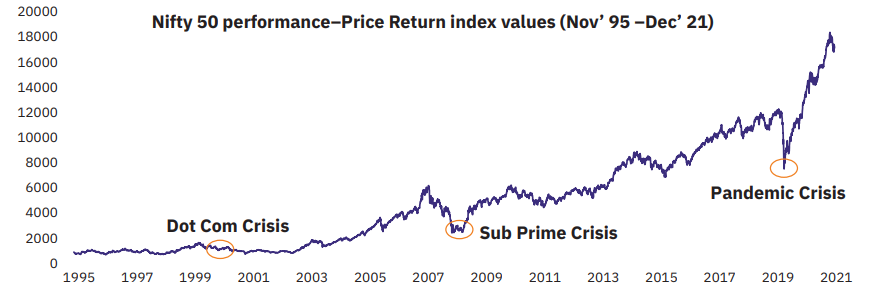

Market timing risk is the biggest fear of every investor, especially while investing a large amount. No one can predict a market crash and the time it takes to recover. The anxiety of a potential loss is the reason many investors hesitate to invest a lump sum. That’s where a Systematic Transfer Plan comes into the picture.

Systematic Transfer Plan (STP) is a way to strategically invest and distribute your lump sum amount in mutual funds. In this blog, we will learn what an STP is, how it works, and how to utilize it to mitigate risk.

What is STP and How Does it Work?

A systematic Transfer Plan is an investment strategy that lets you systematically transfer funds from one mutual fund scheme to another mutual fund scheme. You can invest your lump sum amount in a source fund and periodically transfer it into the target fund(s) in installments. The source fund is usually a debt fund (preferably liquid fund). The target fund(s) can be equity, debt, or a hybrid based on your risk appetite.

Once you park your money in a liquid fund, you can decide the amount and frequency of the installments toward the target fund. Please note that both source and target funds have to be from the same fund house. For example, your source fund can be SBI Liquid Fund and your target fund can be SBI Bluechip Fund.

Types of Systematic Transfer Plan (STP)

Fixed STP: A fixed installment amount decided by the investor to be transferred from the source fund to the target fund at regular intervals (eg: monthly). This method provides a steady and predictable transfer of funds, helping to average out the cost of investment in the target fund.

Flexible STP: In this method, you can change the installment amount as per your preferences. This provides greater flexibility in managing investments, as the transfer amount can be adjusted to take advantage of market opportunities or to respond to changing financial goals.

Capital STP: Instead of transferring the principal, this method transfers the capital gains earned from the market appreciation of the source fund to the target fund, keeping the capital intact

In order to mitigate the market timing risk and achieve a disciplined investment strategy, a fixed STP is ideal.

Benefits of a Systematic Transfer Plan

Risk Management

STP balances out market timing risk by distributing your investments in installments over a specific period. That way, even if you invest a lump sum, you don’t have to worry about investing at the market peak and volatility affecting your entire corpus.

Rupee Cost Averaging

Rupee cost averaging helps in averaging out the purchasing cost of your investment. Let’s say you’re investing INR. 10,000 via STP. You will purchase more units of a mutual fund when the unit price is low and fewer units when the unit price is high. That way, your investment amount remains fixed but the number of units that you acquire changes based on the unit price.

For example: Monthly STP Amount- INR. 10,000

| Unit Price (Fund NAV) | Units Purchased with INR. 10,000 |

| 50 | 200 |

| 60 | 166.6 |

| 65 | 153.84 |

| 62 | 161.29 |

Total amount invested in 4 months = INR. 40,000

Total units purchased = 681.73

Average Unit price = 58.67

Ideal Returns

With STP, you earn returns from both the source as well as target funds. A source fund, usually a liquid fund, can offer higher returns than your savings account. The target fund, either equity or balanced, tends to deliver superior returns over a longer horizon.

Flexibility

You have the flexibility to choose the STP amount, frequency, and number of installments based on your preferences. If you wish to change the STP amount, you can stop the existing STP and easily start a new one.

Diverse and Balanced Portfolio

A systematic transfer plan initially parks your money into low-risk instruments, i.e. debt funds. It reduces the impact of market volatility on the principal amount by transferring it into the target fund over a period of time. Therefore, you’re diversifying your investment with a combination of debt fund (low risk) and equity fund (moderate to high risk), and balancing out your portfolio’s risk.

Now let’s answer the question you must be thinking about after reading the STP features.

How is STP Different From SIP?

A systematic transfer plan (STP) shares some features of the systematic investment plan (SIP).

What is SIP?

A systematic investment plan is a method to transfer a certain amount every month from your savings account to the mutual fund(s) of your choice. You can start SIPs across multiple mutual funds matching your risk profile and financial goals.

Use our SIP calculator to plan your monthly installment to fulfill your goals.

STP vs SIP

In the case of STP, each installment is a withdrawal from a source fund. You can only transfer funds into the target fund(s) of the same mutual fund house. For example, if you want to invest in Quant Small-Cap Fund via STP, you will first park your lumpsum into Quant liquid fund.

SIP, on the other hand, takes place directly from your savings account. You can auto-schedule SIPs from your preferred bank account to any mutual fund of your choice.

Let’s take an example: You have INR 10,00,000 to invest. You can either keep it in your savings account and start an SIP of INR. 20,000. Or you can deploy it into liquid funds and start an STP of INR. 20,000 for the next 4 years.

| Total Investment Amount | Money Kept In | Investment Type | Monthly Investment Amount (for 4 years) | Total Wealth Gained (Interest + Returns on Mutual Funds Avg 12% p.a.) |

| 10,00,000 | Savings Account @ 4% interest rate | SIP | 20,000 | 13,06,636 |

| 10,00,000 | Liquid Fund @ 6.5% interest rate | STP | 20,000 | 13,56,688 |

Your monthly installment of INR. 20,000 will start compounding with the chosen mutual fund. With STP, you earn more interest and generate more overall returns.

When to Choose STP over SIP?

A systematic transfer plan (STP) is ideal to manage your lump sum amount. For example, a large amount that you receive from a gig, by selling a property, your yearly bonus, from PF after retirement, or an inheritance. You’d rather keep that money safe than invest it all into the market at once.

While you can keep it in a savings account and start SIP, a savings account offers a lower interest rate. Instead, a liquid fund or a short-duration debt fund delivers better post-tax returns.

STP is not an alternative to SIP, it’s a companion to SIP. You can have a combination of SIPs and STPs. STP is better for managing large corpus that needs to be deployed monthly instead of in one go. Whereas SIP handles regular monthly investments.

STP vs Lump Sum Investment

What is Lump Sum Investment?

Lump sum investment is a straightforward technique in which you invest a large amount all at once. Investors usually prefer investing a lump sum to capitalize on a market decline or when the market is steadily growing.

However, volatility in the market can affect that entire amount. Therefore, it is usually better to spread out the investment over time to benefit from rupee cost averaging.

| Systematic Transfer Plan | A strategy to systematically transfer your lump sum investment from one mutual fund to another. Park your lumpsum amount in a source fund (liquid fund or short-duration debt fund) Set up an STP to gradually transfer that amount into target mutual fund(s) in regular installments. Benefit from rupee cost averaging. |

| Systematic Investment Plan | A disciplined approach to regularly invest in mutual funds of your choice. Invest in various categories of mutual funds that align with your risk appetite, investment horizon, and financial goals. Start a SIP to regularly transfer a specific amount from your savings account to mutual funds. Benefit from rupee cost averaging. |

| Lump Sum Investment | Investing a large amount at once to capitalize on market decline or upcoming market rally. Ideal only in specific scenarios. |

3 Ideal Scenarios To Use STP for Investing In Mutual Funds

Risk Management During Market Volatility

A systematic transfer plan is ideal to overcome market volatility by spreading out your investment over time. Market movements can be unpredictable. Hence, investing a large amount at once in the market can be risky. STP helps stabilize the risk by gradually transferring funds from the source scheme to the target scheme.

Effectively Managing Surplus Funds

STP comes in handy in managing surplus funds. You can park it in a liquid or short-term debt fund and benefit from higher interest rates than a bank account. These funds can gradually be shifted to an equity-oriented or hybrid fund.

Choosing an ideal target fund depends upon your financial goals and risk appetite. You can take a risk profiling quiz to understand the asset-class concentration suitable for you.

Rebalancing Your Portfolio

STP is often a preferred solution to rebalance your portfolio.

Investors who prefer to maintain a fixed ratio of equity to debt often use STP to periodically rebalance their portfolio. Learn more about asset allocation here.

Investors who are nearing retirement also use STP to gradually shift their equity investments to safer debt instruments.

Factors to Consider Before Starting an STP

Market Conditions

It is crucial to analyze market conditions before investing. However, you shouldn’t try to time the market. It often doesn’t work in anyone’s favor. Instead, get an idea of the current yield of debt funds and choose a suitable target fund matching your financial preferences. Savvy investors prefer to start STPs and SIPs in a sideways or bearish market to acquire units at lower prices. You can reach out to VNN Wealth to strategically plan your STPs.

Taxation and Exit Load

Each installment from the debt fund (source fund) to the equity or equity-oriented fund (target fund) is considered a withdrawal from the debt fund. Therefore, you will have to pay capital gain tax on each STP installment.

You will also have to pay capital gain tax on withdrawals from the target fund. The tax will depend upon when you withdraw funds. A short-term capital gain tax of 20% is applicable for investments redeemed within 12 months of investment. Otherwise, you’ll have to pay a 12.5% capital gain tax above 1.25 lakhs on investments redeemed after 12 months.

Psychological Factors

A lot of investors get anxious with uncertainties in the market. A volatile market can trigger decisions against the growth of your investment. Once you start a systematic transfer plan, do not worry about market volatility. Pausing STPs and SIPs in fear of expensive markets can break the flow of your investment strategy. So don’t let your emotions such as fear or greed come in between your portfolio’s growth.

Who Should Choose a Systematic Transfer Plan (STP)?

1. Mitigating Equity Market Risks: Conservative Investors looking to participate in the equity market while minimizing risk on investment.

2. Strategic Lumpsum Investment: Individuals who have received a lump sum amount (for example, payment from a project, bonus, inheritance, retirement fund, etc) and want to systematically invest it. STP is ideal for freelancers/self-employed individuals or professionals practicing on their own such as doctors, lawyers, etc. Or for salaried professionals who have received a yearly bonus, or sold property.

3. Portfolio Rebalancing: Investors seeking to rebalance their equity and debt exposure but want to do it over a period of time and not in one switch.

How to Create STP?

In order to create an STP, you first have to choose the target fund. The target funds depend upon your risk profile, financial goals, existing investments, etc. An experienced financial advisor will help you choose the right funds to add to your portfolio.

Reach out to VNN Wealth to evaluate your portfolio.

Once you choose the target fund, you have to park your lumpsum in a liquid fund of the same mutual fund house. Afterward, you can gradually transfer the funds into the chosen target fund.

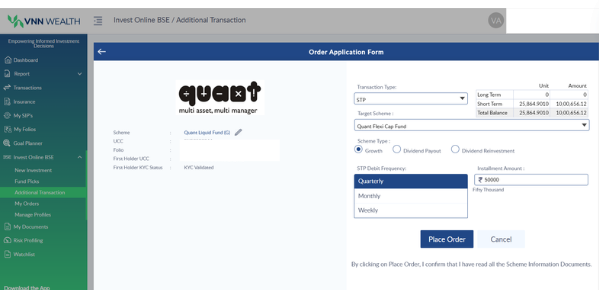

You can easily create an STP with VNN Wealth. Here’s a step-by-step process.

1. Login to the VNN Wealth portal and make sure your KYC process is completed.

2. Navigate to ‘Invest Online BSE’ from the side menu.

3. Locate ‘New Investment’- Choose a liquid fund to park your lump sum. For example, Quant liquid fund. Click on Transact and complete the lump sum investment.

4. Then, locate ‘Additional Transaction’ under the same menu. Find your liquid fund investment and click on transact.

5. Select the transaction type- in this case, STP.

6. Choose your target scheme. For example, Quant Flexi Cap Fund.

7. Select ‘Growth’ as your scheme type.

8. Now set the frequency, amount of STP, and start date (or number of installments).

9. Confirm all the details and place your order.

While you can do this on your own, our team is happy to assist you in setting STP. Contact VNN Wealth for further guidance.

Conclusion

A Systematic Transfer Plan (STP) is a disciplined investment approach. Investors aiming to mitigate market timing risk and optimize their lump sum investments in a volatile market can choose STP. The combination of debt funds and equity funds offers diversification and risk balancing to your existing portfolio. STP offers SIP-like features to the lump sum investment. You can benefit from rupee cost averaging and mitigate market volatility by distributing your investment over time. STP also helps you gradually rebalance your portfolio without having to sell your investments.

So next time you’re wary of investing a lumpsum amount, choose a systematic transfer plan.

Start your STP Today!

Are you seeking an investment avenue to park a lump sum but are scared of market volatility? Book a call back from our experts and seamlessly start your STP today. Explore our products and don’t forget to review your portfolio before investing.