Portfolio Management Service (PMS) offers customized portfolio management for high-net-worth individuals and Non-individuals such as HUFs, partnerships firms, sole proprietorship firms and body corporate.

A skilled portfolio manager handles your portfolio, which can be crafted as per your financial goals and objectives.

When you invest in a mutual fund, your money goes to the fund house and then into the fund. However, in PMS, the transactions take place through your demat account. Therefore, you can see all the transactions happening on your behalf.

You may like to read- Basics of Portfolio Management Service before moving ahead.

When is the Right Time to invest via Portfolio Management Service?

1. More than 50 Lakhs of Portfolio to Manage

PMS caters to HNIs with a minimum of 50 lakhs (as per SEBI guidelines) of investment.

After spending years with mutual fund investments, you may have gotten comfortable with the risk associated with it. Now, if you don’t mind a slight more risk for even better rewards, PMS can be your next step.

Pro Tip- Entrust a PMS house with 50 lakhs only if that amount is not more than 20% of your overall portfolio.

2. Managing a Large Number of Stocks

Recently, especially right after COVID, we reviewed a lot of portfolios with a large number of stock holdings.

At a certain point, losing track of all these stocks is bound to happen. Investors may not have enough time to study the performance of each company in the current market. This leads to a long tail of underperforming stocks.

The declining performance of multiple stocks creates a significant dent in your overall portfolio return.

Instead, you could invest in stocks that align with your risk appetite and goal by selling underperforming stocks.

Experts at PMS House can help you manage all your stock holdings. You can convey your buy/sell preferences and the portfolio manager will re-shape your portfolio accordingly.

3. ESOPs Holdings

Salaried individuals may have ESOP holdings over the years.

While reviewing client portfolios, we’ve often noticed that the biggest holding in their overall portfolio belongs to ESOP. Sometimes 90% of the portfolio consists of a single ESOP.

This leads to high-concentration risk. The returns will depend on the performance of a single ESOP. Your portfolio may not beat the benchmark.

With PMS, you can filter out the stocks you want to keep or sell. You can set your preferences and invest accordingly.

For example, if you already hold an ESOP of Infosys, you can avoid buying more stocks of the same company. That way, you can truly optimize your portfolio.

A well-balanced and diverse PMS commonly holds 20-30 concentrated stocks. Portfolio managers will readjust your portfolio accordingly by buying/selling stocks. The right asset allocation can minimize the risk and maximize returns.

4. Flexibility

PMS offer more flexibility compared to mutual funds.

Mutual fund categories have to follow SEBI regulations on asset allocation. But also, there are many norms regarding the capping on the underlying stocks, bonds and cash holdings. Additionally, mutual funds do not have exposure to the unlisted stocks.

PMS can choose the asset composition as per investor’s preferences and market opportunities. You can have a concentrated portfolio of 20-30 stocks.

If you are someone who follows Sharia law, you can avoid investing in alcohol, tobacco, gambling, gold, and silver trading, banking and financials, pork and non-vegetarian, advertising, media, and entertainment industries.

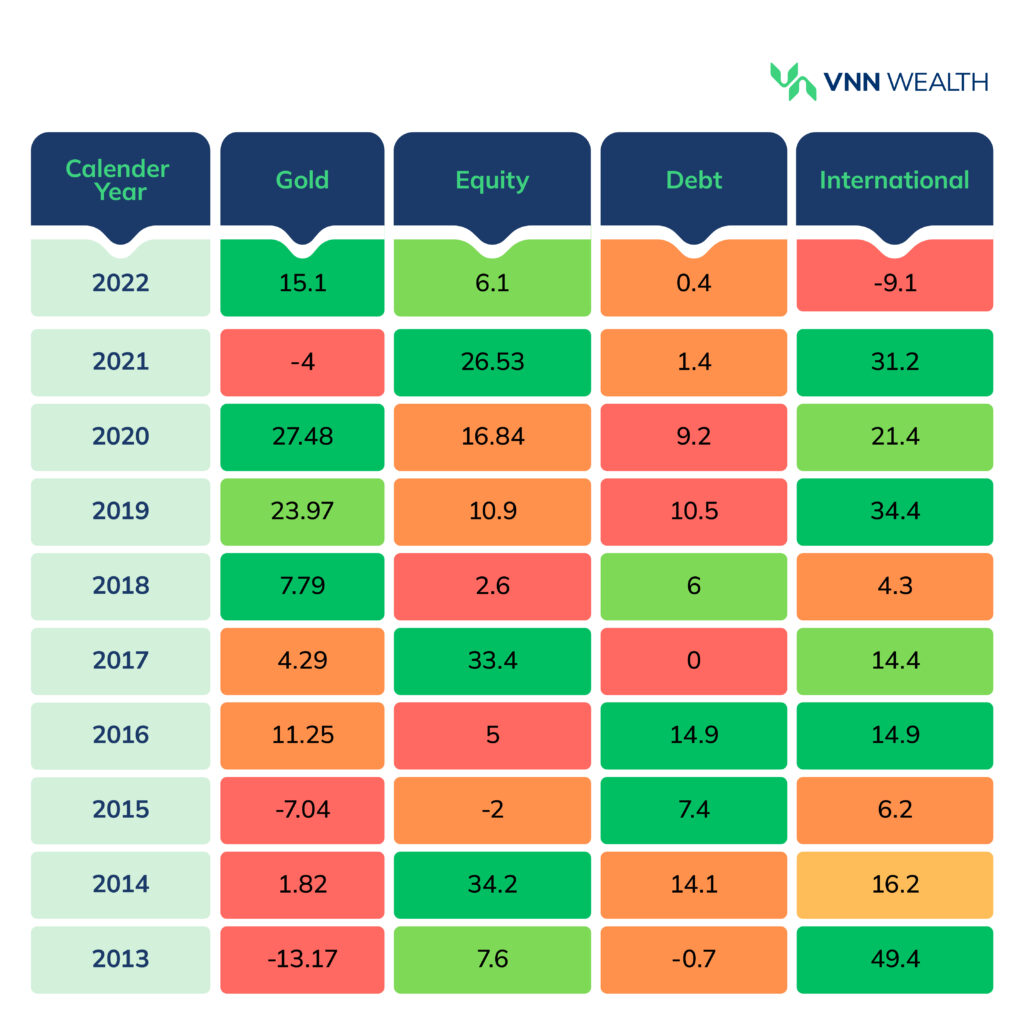

It is possible to invest beyond equity, debt, and gold. PMS can open a door towards alternative assets and sectors to invest as per your choice.

How to Select a Good Portfolio Management Service?

Launching a PMS in India is much easier than launching a mutual fund. Therefore, there are a lot more PMSs to choose from.

Without a wealth manager by your side, it would be difficult to narrow down your choices. A certified wealth manager/relationship manager can recommend a list of suitable PMSs. Get in touch with VNN Wealth to know more.

Once you have a bunch of options ready, here’s what to review in a PMS.

1. Evaluate the Credibility of a PMS

Make sure the PMS is registered with SEBI (Securities and Exchange Board of India). Head to their website to review their team’s experience and track record.

Delivering successful results in various economic cycles is a sign of a good PMS.

2. Communication and Transparency

The whole point of having a custom portfolio is knowing what’s happening with it. Having an active communication right from the start is the key to assessing the PMS provider.

Make sure you read the client testimonials on their site. Ask questions about strategies. See the response time and quality. As an informed investor, it is your duty and right to know everything.

3. Fee Structure

PMSs either charge a fixed management fee and an exit load or a profit participation fee. Each PMS has a different fee structure. To give you an idea, the fixed management fee could be between 2 to 2.5% of the total asset value. The exit load depends on the holding period and withdrawal value and could range from 1 to 2.25%.

The profit participation fee depends on the agreement you have with the portfolio manager. For example, the portfolio manager will share a small part of your profit if it crosses a hurdle rate of 10-12% p.a. return.

It is crucial to understand the fee structure before you hand over your portfolio.

4. Strategies and Risk Management

As mentioned above, PMS customizes your portfolio as per your financial goals and the timeframe in which you want to achieve them.

Therefore, the investment strategy and risk management changes as per the investor’s risk appetite.

Similar to mutual funds, PMS also offers large-cap, mid-cap oriented investment options. You can build a strategy to meet your financial requirements and preferences.

Your wealth manager will be able to guide you through the entire process. If you don’t have a wealth manager yet or want to hire a new one, VNN Wealth is just a phone call away.

Final Words

According to SEBI data, the assets under management of PMS have increased to 28.50 lakh crore by 2023, with 14% year-on-year growth.

Many investors are actively seeking personalized investment opportunities to align with their financial goals. If planned right, PMS can offer superior returns compared to conventional investment avenues.

If your portfolio meets the criteria mentioned in this article, you can definitely go for PMS.

Take a complimentary portfolio analysis with VNN Wealth to know where your portfolio stands and which PMS to choose. Contact us to know more.

Follow @vnnwealth for more insights in the world of finance.