Mutual funds are the best way of building wealth and earning a fixed income from it. Be it a lump sum investment or SIP, mutual funds will deliver superior returns in the long term.

And once you have enough wealth built, you can start earning income from your mutual funds.

There are two ways of earning a fixed income from your investments:

- Systematic Withdrawal Plan (SWP)

- Income Distribution Cum Capital Withdrawal Plan (Previously known as Dividend Plan.)

Let’s compare both in detail.

How Does a Systematic Withdrawal Plan Work?

A Systematic Withdrawal Plan (SWP) is an automated way of withdrawing a fixed amount from your mutual funds at regular intervals. Investors can define the amount and frequency at which they want to earn income.

To put it simply, SWP is the opposite of a Systematic Investment Plan (SIP). In SIP, a predefined amount goes from your savings account to a mutual fund of your choice. SWP plan sells units of your mutual funds and transfers the amount to your bank account.

Pro Tip- SWP is more effective when you give time to your fund to grow and benefit from the power of compounding. Stay invested for a longer duration. Once you have enough wealth built, you can start a SWP. It is one of the most tax-efficient ways to generate a consistent inflow, especially post-retirement.

How Does The Income Distribution Cum Capital Withdrawal Plan Work?

In the IDCW (Dividend) plan, investors periodically receive a profit made by the fund. The mutual fund dividend plan works differently than the stock dividend.

In the case of mutual funds, the unit price increases with capital appreciation, interest earned on bonds, and dividends. Therefore, the income received is not like the dividend from a stock but your own profit.

Example:

The unit price (NAV) of a mutual fund is INR 100. After capital appreciation, bond interest, and dividends, the price goes up to INR 120.

Now, if the mutual fund declares a dividend of INR 10 per unit, you will receive the amount (INR. 10 x No. of units) in your account but the NAV will go down to 110.

Let’s say you have purchased 1000 units of a mutual fund with an NAV of 100/unit. You will end up investing INR 1,00,000 in an IDCW mutual fund.

|

Total Amount Invested

|

1,00,000

|

|

Unit Price

|

100

|

|

Units Assigned

|

1000

|

|

Updated Unit price after capital appreciation, bond interest, and dividends

|

120

|

|

Total Amount in a Fund

|

1,20,000

|

|

Dividend Declared

|

10 per unit

|

|

Dividend Amount Received (Dividend x Number of units)

|

10 x 1000 = 10000

|

|

Updated NAV after Dividend Payout (Previous NAV – Dividend)

|

120-10= 110

|

|

Remaining Invested Amount in a Fund (Updated NAV x Number of Units)

|

110 x 1000 = 1,10,000

|

The income investors earn from the IDCW plan is pulled out of the profit from their own investments.

In the case of stocks, investors receive the dividend as an additional payout over and above the appreciated capital. Therefore, neither the principal amount nor the earned profit is reduced after dividend payouts.

But with IDCW mutual funds, the appreciated amount goes down after the payout. This created confusion among investors. Therefore, SEBI renamed the Mutual fund dividend plan to Income Distribution Cum Capital Withdrawal Plan for clarity.

In the IDCW plan, investors do not get to choose the amount or frequency of the payout. Therefore, it’s a less flexible plan compared to SWP.

A quick overview of SWP vs IDCW 👇

SWP vs IDCW Plan: Top 3 Differences

1. Flexibility of Choosing the Fixed Income

A systematic Withdrawal Plan allows investors to select the payout amount, frequency, and date. IDCW, on the other hand, depends on mutual fund performance and the fund house’s decisions.

Let’s say you start an SIP of 20000 at 12% p.a.

You will accumulate:

- 26,39,580 in 7 years.

- 46,46,782 in 10 years.

- 1,00,91,520 in 15 years.

- 1,99,82,958 in 20 years

The SIP amount and horizon depend on your financial goals.

Now, after 20 years you can comfortably withdraw 1L/month as a regular income for the next 20 years via SWP.

The remaining amount will keep compounding.

It is clear that SWP offers more flexibility compared to a dividend plan. It also helps you plan a source of income ahead of time.

2. Surety of Receiving the Income

Receiving a payment via the IDCW plan depends on decisions made by the fund houses. The frequency and amount may change as per the fund’s performance.

SWP, on the other hand, offers surety of payouts. You have full control over when you want to start SWP, for what amount, and how often.

You will receive the income irrespective of market conditions.

3. SWP vs IDCW: Tax Implications

One of the important factors to consider before choosing an income plan is the applicable tax.

Dividends are a form of income, therefore, will be taxed as per your tax slab. So, if you fall under higher tax brackets, a dividend plan may not be ideal for you.

Systematic Withdrawals are a form of mutual fund redemptions. Taxation on mutual fund redemption depends on the holding period.

- If you start SWP within 12 months of your investment, you will attract a 20% Short-Term Capital Gain tax on your withdrawals.

- Holding your investment for more than 12 months will attract a 12.5% Long-Term capital gain tax on withdrawals above 1.25 Lakhs in a financial year.

Therefore, SWP becomes a more tax-efficient fixed-income avenue than a dividend plan.

Note- It is always better to hold your mutual fund investments for a longer duration. Not only is it tax efficient, but also helps you accumulate larger wealth by the power of compounding.

Which Fixed Income Option Should You Choose Between the Two?

Investors who do not rely on income from mutual funds but wouldn’t mind a periodic payout often go for the IDCW plan. It is not their primary mode of generating regular income.

IDCW plan does not wait for the principal amount to grow by compounding. Therefore, many investors prefer the growth plan.

SWP is suitable for investors looking to generate regular income on their own terms. It offers more flexibility and tax-efficient withdrawals. It is advisable to let your money grow for years and then start the SWP.

Choosing a suitable plan entirely depends upon your financial goals and preferences.

Final Thoughts on SWP vs IDCW

To answer the primary questions- SWP vs IDCW (Dividend): Which one is better for regular income from mutual funds?

SWP is the clear winner because it gives you the freedom to choose the amount and frequency. The income withdrawn via SWP is more tax-efficient than the dividend income. Investors wanting to earn a salary even after retirement should go for SWP.

It is wise to have clear financial goals to select the right plan. If you have any further queries, feel free to reach out to us. Experts from VNN Wealth would be happy to help you shape your investment portfolio.

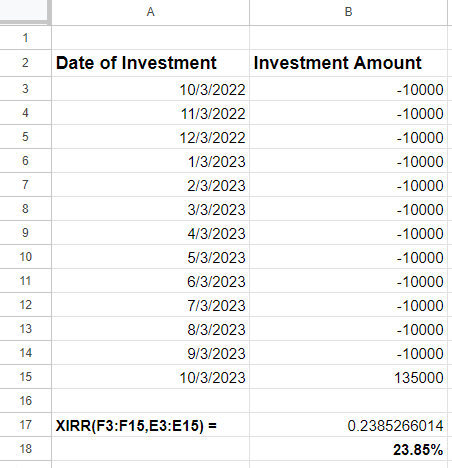

The negative sign in front of each investment indicates cash outflow.

Your monthly investment amount and dates could vary. In such cases, the XIRR formula gives the accurate calculation of returns.

The negative sign in front of each investment indicates cash outflow.

Your monthly investment amount and dates could vary. In such cases, the XIRR formula gives the accurate calculation of returns.