The biggest obstacle between you and your financial goals is- You! Your emotional investing is causing more harm to your portfolio than you realize.

In an ever-changing financial landscape, it’s easy to let emotions influence your decision. You’re a human after all.

But… Your fear, greed, and overconfidence, are clouding your judgment, pushing you towards making an irrational decision.

Strong portfolios and successful investments require discipline and emotional stability. And if a small part of you feels you’ve allowed your emotions to overpower your decisions, then this blog is for you.

Keep reading as we’ll explore how emotions can impact investment and simple strategies to keep them in check.

We let our emotions control the situation in almost everything in our lives. Instead of relying on logic or data, we let our feelings make the decision for us. We do the same with investments.

Does any of the following sound familiar?

Fear: In fear of losses, you end up selling your investments during a market dip.

Greed: Taking unnecessary risk by chasing the returns during a market rally.

Overconfidence: Trying to time the market, leads to impulse decisions.

FOMO: Fear of missing out on the market trends.

Regret: Irrational decisions in the hope of covering the previous losses.

Here are some of the examples that may also sound familiar:

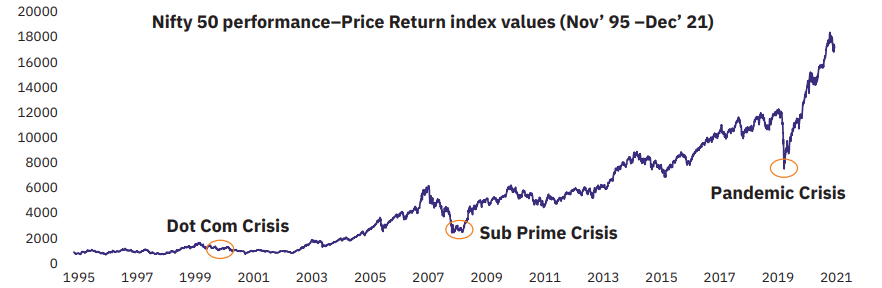

When the market crashed during COVID-19, a lot of investors cashed out their portfolios in fear of losses. However, the market rallied up soon after. The Nifty 50 went up by 124% between April 2020 to Oct 2021.

Similarly, in 2008, Sensex experienced its biggest crash in January and continued to decline for the rest of the year. Investors sold significant portions of their investments to avoid further loss. Sensex recovery took more than a year. During this crisis, patient investors survived but emotional investors caused a huge dent in their portfolio.

Market crashes are temporary and markets always eventually recover. During these tough times, your actions can make or break your portfolio.

People often let several psychological biases alter their investments. These biases arise from the need to stay in control of your money. We’ve noticed one or the other of the following psychological traps clouding the decisions of the investors we meet.

The most common trap that people fall into is following the crowd. From buying a car to careers and investments, people tend to follow others.

For example, during the dot-com bubble, everybody invested in tech stocks and lost significant wealth when the bubble burst in 2000.

The backbone of this herd mentality is fear of missing out. People want to jump on the bandwagon with others, follow the same path. However, what works for others may or may not work for them.

Everyone’s financial situation and investment goals are different. Therefore, as comforting as it appears, following others while investing does more harm than good.

Studies show that investors tend to feel the pain of losses more deeply compared to the joy of gains. The fear of losses prompts premature selling during the market dips.

We’ve met plenty of investors who, despite a defined time horizon for their investments, get restless with temporary loss.

What these investors fail to understand is, that market corrections aren’t going to last forever. As the economy grows, the markets eventually follow. Therefore, market volatility can be mitigated by time.

As you can see in the graph above, every market crash was eventually recovered. You need to be patient. Your investments deserve time to recover from the losses. Don’t let the temporary loss get in the way of your long-term growth plan.

People always try to make sense of their decisions by selective information. They want to believe in what they want.

For example, someone who is convinced that real estate is the best investment option will only focus on success stories. They’ll only pay attention to rising real estate prices in certain areas. Or positive experiences of their friends. Their upbringing and their family’s beliefs also play a role. These people only see what they want to see and completely overlook risks like market downturns, maintenance costs, or long periods with no rental income.

They try to seek information that aligns with their beliefs. This bias leads to misinformed decisions.

You’re trying to build wealth to make your financial future secure. You should trust relevant data to make an informed decision.

Disciplined investment is the key. Having clear financial goals will help you stay focused, even during market uncertainties.

Here’s what you need to do:

Step 1: Define your goals. For example, buying a car next year. Moving into a new house in two years. Or retiring early. Assign a tentative amount to each goal that you’ll need to generate.

Step 2: Evaluate your financial situation. Get all your statements and note down your monthly expenses, EMIs, funds you’re keeping for emergencies, salary increments, etc. This will help you set aside an amount you can invest every month.

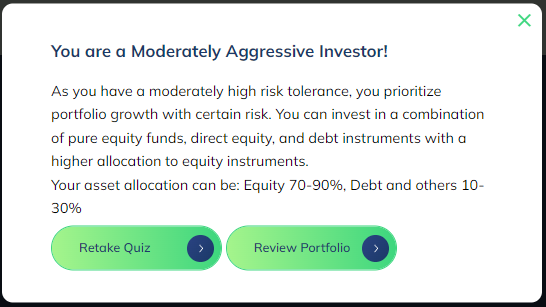

Step 3: Take a risk profiling quiz to understand your investment personality on the spectrum of aggressive to conservative. Many investors like to believe (or pretend) they’re aggressive investors. However, the kind of risk you’re willing to take and the risk you can actually take is different. So answer honestly and the quiz will give you the suitable allocation of equity, debt, and other instruments. For example👇

Step 4: Evaluate your investment portfolio. Review your current holdings and realign them as per your risk profile.

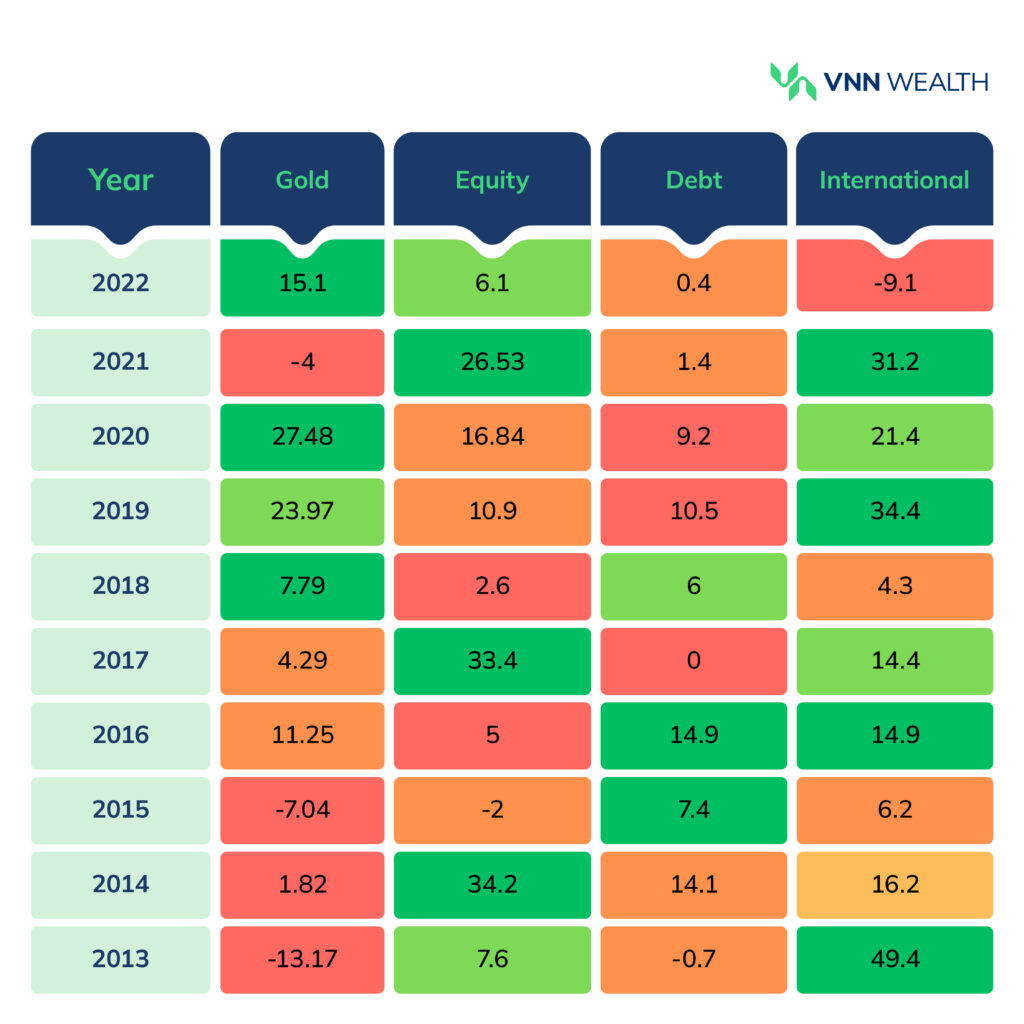

Asset allocation is crucial to maintaining a diverse portfolio and balancing risk. Equity, debt, and gold each experience a different cycle every year. However, they complement each other.

Take a look at the table below. The performance of each asset class varied every year.

So if you are worried about your portfolio crashing, don’t invest heavily in one asset class. That’ll lead to high-concentration risk. Instead, distribute your money across different instruments to balance the risk. That way, you won’t be tempted to make any impulse decisions.

Let’s take a simple example. Baking a cake requires a specific amount of time to cook completely. If you take it out of the oven before the timer finishes, you’ll be greeted by an undercooked cake.

Similarly, when you invest money in an instrument, it needs a specific time to deliver returns. Premature withdrawal will cause a loss.

So, when you define goals, you must assign a timeline for each. For example, buying a house in two years.

Since your time horizon is only two years, investing in small-cap or mid-cap funds would be silly. These funds need 5+ years to deliver optimal returns. Instead, you can invest in debt funds with a suitable horizon. On the other hand, your time horizon would be longer to achieve your retirement goals. In that case, you should definitely invest in high-risk funds.

Because…risk is not defined by a fund category but by a time horizon. Each mutual fund category has a pre-defined time to mitigate short-term volatility.

| Goal | Timeline | Mutual Fund Category |

| Buying a car | Within 3 to 6 months | Low-Duration Debt Funds such as: Kotak Low Duration Fund Axis Treasury Advantage Fund SBI Magnum Low Duration Fund |

| Moving into a new house | In 3 years | Dynamic Bond Funds / Banking and PSU Funds / Hybrid Funds like Balanced Advantage Funds, Multi-Asset Funds: ICICI Prudential Balanced Advantage Fund Kotak Balanced Advantage Fund Quant Multi Asset Fund |

| Wedding | In 3 to 5 years | Large Cap Funds such as: Nippon India Large Cap Fund ICICI Prudential Bluechip Fund SBI Bluechip Fund |

| Children’s Education | Within 5 to 7 years | Mid Cap Funds such as: Quant Midcap Fund Motilal Oswal Midcap Fund HDFC Midcap Opportunities Fund |

| Retirement Planning | 7 Years and Above | Small Cap Funds such as: Nippon India Small Cap Fund Quant Small Cap Fund TATA small cap Fund |

Important: The above table only illustrates time-based investments. However, you also need to consider other parameters such as your risk appetite, the fund’s rolling returns (consistency), and your overall investment portfolio. Choose funds that align with your objectives and contribute to the growth of your overall portfolio.

Automation removes the temptation of timing the market. It helps you consistently invest toward your goals. You can set up an SIP (Systematic Investment Plan) for mutual funds of your choice.

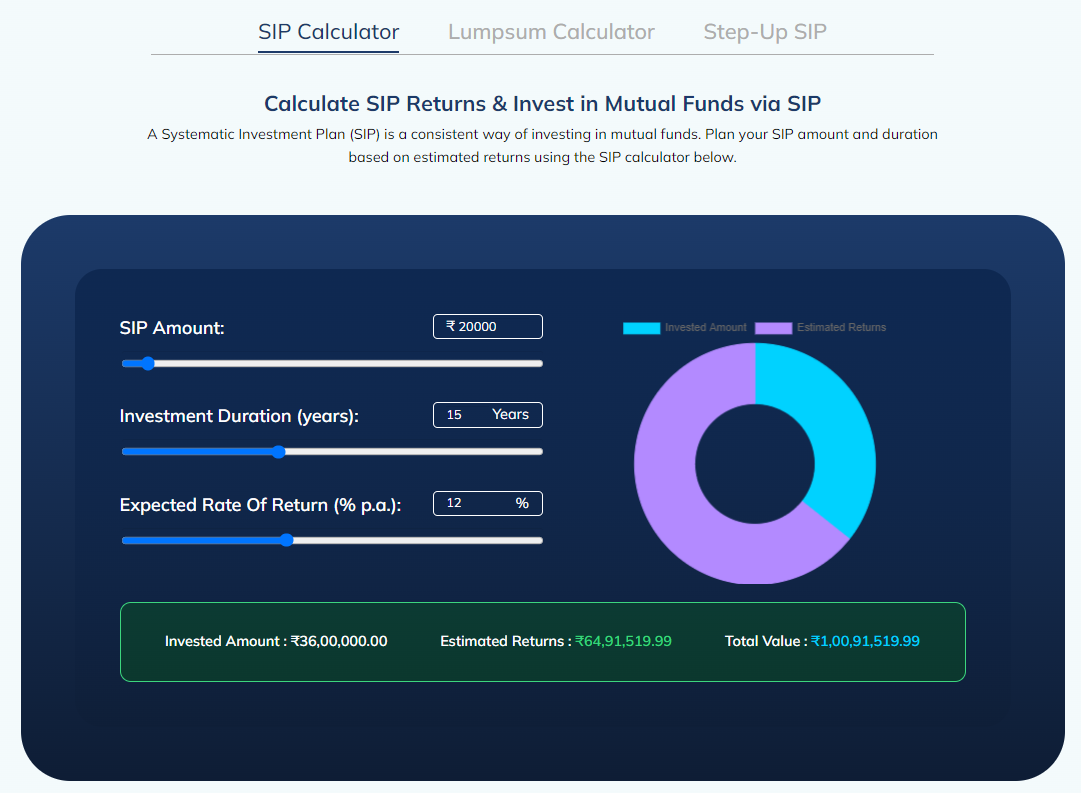

Here’s how disciplined consistent investment can compound over a period of time. Let’s say you aim to accumulate 1 crore for your child's college education over the next 15 years. By consistently investing INR 20,000 per month in mutual funds, with an expected average annual return of 12%, you can reach this financial goal within 15 years.

You can play around with numbers using our SIP calculator to set a specific timeline for your financial goals. Automate your SIP installments and let the money compound on its own.

A professional financial expert will objectively evaluate your investments. They will provide data-driven insights to strengthen your portfolio irrespective of the market conditions.

A professional financial expert can:

Analyze your risk appetite and review your portfolio.

Assist you in choosing the right mutual funds.

Ensure your portfolio’s risk aligns with your risk profile.

Help you identify redundant investments and ensure true diversification.

Guide you through the market volatility.

So, even if you’re a savvy investor with market knowledge, an expert can shed light on the situation from a different angle.

If you want to review your portfolio and discuss your investment strategy, book an appointment with us. We will assist you throughout.

Emotional Investor Rahul often gets anxious about market uncertainties. He constantly monitors his portfolio and complains about poor returns. He ended up investing in multiple stocks due to a trend his friend was following and sold it at a loss when the stock price began declining. His patience runs out after every minor change in the market and he starts panic selling or impulse purchasing. He claims to be an aggressive investor but never bothers evaluating his actual risk appetite.

In contrast, Pratiksha, a Rational Investor always focuses on a long-term picture. She invested in various asset classes for diversification and follows a strategy based on her risk appetite. While her portfolio also goes through ups and downs, she is not concerned. She keeps investing via SIP for a defined horizon and lets the money compound. She quarterly monitors her investments only to see where it is going and talks to an expert if she has any questions.

Outcome? Pratiksha’s consistency and data-driven approach will outperform Rahul’s emotional investing. While Rahul might make quick gains sometimes, these wins are unpredictable.

Therefore, always stick to an investment strategy catering to both short-term and long-term goals.

Acknowledge your mistake: Start by accepting your mistake. Identify the situations where you let your emotions run wild. Moving forward, you can stop yourself from making the same mistake again.

Re-evaluate your portfolio: It’s never too late to fix any errors. Re-evaluate your portfolio with an expert- identify gaps, poor-performing assets, redundant investments, etc. Sell the assets that are consistently delivering poor returns. Reallocate your money to asset classes that’ll deliver returns ideal for your financial goals.

Focus on consistency: Encourage yourself to focus on disciplined investment. Plan Systematic Investments via SIPs or STPs. That way, you will invest a small amount every month and benefit from compounding.

Keep your emotions in check: If you feel stressed about your investments, try to have a long-term perspective. Some stress management techniques such as meditation, exercise, or hobbies can help you navigate your emotions. It’s easy to worry when the market is fluctuating. But, focus on what you’re trying to achieve with your investment so you won’t get side-tracked.

Emotional investing can be detrimental to your long-term financial success. Fear, greed, ego, overconfidence- all these emotions push you in the wrong direction. Instead, unlock your emotional intelligence to make logical, goal-oriented investment decisions.

As Daniel Kahneman says in his book Thinking, Fast and Slow- emotional decisions can be impulsive whereas rational decisions require more thought.

So, this is your sign to rethink your financial decisions. Make the right choice by creating a strategy for better returns. Have a long-term perspective than a short-term panic. Start making small changes today and you’ll notice the results in due time.

Are you ready to give your investment portfolio another chance?

1: Take a risk profiling quiz to determine your portfolio's ideal asset allocation.

2: Review your portfolio and choose the right mutual funds.

3: Sign up or log in to start investing. Effortlessly automate your SIPs and STPs.

If you’re interested in exploring wider investment instruments such as unlisted shares, AIFs, and PMS, reach out to us. VNN Wealth is a trusted wealth management firm in Pune with exclusive investment opportunities tailored to your financial objectives.